Is Bitcoin a Safe Haven? Part 2

Exploring the Volatility of Bitcoin

Introduction

In recent years, cryptocurrencies, most notably Bitcoin, grew in popularity, and

investors have become increasingly concerned about its possible impact on other

asset classes due to its extreme volatility. Understanding the mechanisms of

volatility spillover1 between Bitcoin and traditional assets is critical for investors

looking to diversify and manage their risks.

The volatility of Bitcoin and other cryptocurrencies has been analyzed by

economists and scholars, who have compared it to that of traditional assets. To

determine if Bitcoin’s volatility affects traditional assets and to capture the com-

plexities of volatility spillover dynamics, researchers have used various methods

to investigate market contagion effects.

Several studies have investigated the market contagion effects of cryptocur-

rencies, including Bitcoin, and traditional assets using methods such as GARCH,

wavelet analysis, and DCC-GARCH. Kumar and Suvvari (2019)[KS19] and

Ozdemir (2022)[O18] found evidence of volatility spillover risks among cryp-

tocurrencies, which increased during moments of heightened market uncertainty

and the COVID-19 pandemic era. Other studies have investigated the market

contagion effects of stock and currency rate volatility in oil-exporting countries,

discovering significant volatility spillover impact between stock and exchange rate markets (Mikhaylov, 2018[Mik18]) and considerable spillover effects be-

tween financial markets, including stocks, bonds, and currency rates, especially

during times of financial crisis (Xiong and Han, 2015[Xio15]).

In Guz and Isabetli Fidan’s (2022) study, asymmetric volatility and lever-

age effects were found in five cryptocurrencies, including Bitcoin, driven by

market circumstances such as trade volume and liquidity. Kumar and Ajaz

(2019)[KS19] found substantial co-movement between many cryptocurrencies,

including Bitcoin, using wavelet analysis. Chi and Has (2020)[CH20] discovered

that the GARCH model was the best for predicting Bitcoin volatility using data

from spot and option markets.

This study aims to investigate the volatility spillover effects between Bitcoin

and traditional assets using various methodologies to capture the complexity

of the dynamics. We will assess the hedging effectiveness using Ederington’s

(1979)[Ede79] methodology and implement the hedge ratios technique proposed

by Kroner and Sultan (1993)[KS93] to optimize the allocation of assets in the

portfolio to minimize risk. Finally, we will analyze the statistics of the hedging

effectiveness measure using the methodology proposed by Antonakakis et al.

(2020)[ACG20] to provide insight into the investment strategies and hedging

effectiveness of the portfolio.

In a previous article in this series, we sought to answer the question ”Is

Bitcoin a Safe Haven?”2 by examining the connectedness relationships between

Bitcoin and traditional assets. The study was conducted over the period of 2017-

2022 and found that Bitcoin was becoming increasingly influenced by other

variables such as the NASDAQ Composite Index, the US Dollar Index, and

the CBOE Volatility Index. Our analysis of Bitcoin’s effect on these variables

during its peak period of 2020-2021 led us to question the link between Bitcoin’s

volatility or risk and these variables. As a result, we concluded that Bitcoin

cannot be considered a diversification or safety agent in relation to the assets

evaluated in this study.

The previous study highlighted the importance of understanding the volatil-

ity spillover effects between Bitcoin and traditional assets. In this current study,

we aim to investigate these effects further by using various methodologies to

capture the complexity of the dynamics.

Overall, this research will be useful for investors in understanding the risk

and diversification benefits of adding Bitcoin to their portfolios and the potential

risks and uncertainties associated with these assets. The findings suggest that

volatility transmission effects can vary depending on market conditions and

events.

Empirical methodology

We aim to capture the complexities of cross-market volatility dynamics using

various methodologies. We begin by using the Dynamic Total Connectedness

analysis technique, which allows us to assess the degree of connectedness between

assets in the system. This method helps us to identify which assets play a critical role in transmitting shocks across the network.

We also use the Net Total Directional Connectedness measure (N ETi), which

provides insight into the net effect of a given asset on the network. A positive

value indicates that the asset is a net shock transmitter, while a negative value

suggests that it is a net shock receiver.

Additionally, we employ the Net Pairwise Directional Connectedness mea-

sure (N P SOij ), which allows us to assess whether one asset has a larger impact

on another asset than the other way around. This method helps us to identify

the directionality of the transmission of shocks across the network.

The DCC-GARCH model enables us to examine the total connectedness

index (T CI), which is separated into total directional connectivity ”textitTO

others” and ”textitFROM others”. We may estimate the degree of interconnec-

tivity between assets in the system by studying the T CI. Moreover, we will

re-plot the total connectedness index (T CI), total directional connectivity ”TO

others” and ”FROM others,” and net total directional connectivity (N ET i).

Additionally, we use the network diagrams to visualize the relationships

between assets in the system. The network plots display the NPDC and the

Percentage Change in Connectivity (PCI), which help us to identify changes in

the relationships between assets over time. We also use the net influence index

(INF), which emphasizes percentage changes in the relationships between assets

rather than levels.

To further our understanding, we use the Multivariate Portfolios technique,

which helps us to identify a minimum connectedness portfolio. This technique

allows us to construct portfolios that are optimized for risk management by

minimizing the transmission of shocks across the network. We also look at the

Cumulative Returns of Minimal Connectedness Portfolio, which provides insight

into the performance of the portfolio over time.

We assess the effectiveness of hedging by comparing the returns of a hedged

portfolio to an unhedged portfolio. We also use the hedge ratios technique to

optimize the allocation of assets in the portfolio and minimize risk.

Finally, we analyze the statistics of the hedging effectiveness measure using

a methodology that provides insight into the investment strategies and effec-

tiveness of the portfolio’s hedging.

Data set and empirical results

Data Description

We conduct an analysis of implied volatility, more specifically on BTC price

volatility, as well as examining several other indices such as Dow, NAQ, precious

metals (Gold ETF), currency pairs (DXY), crude oil prices (WTI), and market

volatility (VIX). The time series data utilized for this study encompasses the

period from 2017 to 2022, allowing us to observe the transformative trends in

Bitcoin over the last five years. This methodology not only sheds light on the

dynamics of Bitcoin’s implied volatility but also unveils insights into the broader market landscape, emphasizing the interconnections among diverse asset classes.

The data in the sample is a time series of daily data from 2017 to 2022.This

time period spans the previous five years of Bitcoin variations, from its apparent

maturation to the recent explosion in activity and broad acceptance of the

”currency.”

Empirical Results

We begin by analyzing the Total Connectedness Index (TCI), which evalu-

ates the impact of all factors on the forecast error variance of a single variable

over time. The table displays the percentage connectedness impact between

different variables, with each row representing the impact one variable has on

another. The end column labeled ”TO” shows the impact of other variables

on a specific variable, while the end row labeled ”FROM” shows the impact

of a specific variable on other variables. The penultimate row, labeled ”NET,”

represents the difference between the TO and FROM columns, and the last row

labeled ”NPT” shows how many series a specific series dominates. This table

provides valuable information for analyzing the relationships between different

variables and their impacts on one another.

The results reveal that Bitcoin (BTC) has a minor or negligible effect on

the other series studied, and vice versa. The average influence of BTC on

the other variables in the series is approximately 15%. Additionally, the TCI

graph shows that BTC has an average influence of 20-30% on the other variables

analyzed, with a peak influence of 60% at the beginning of 2020 and an average of

around 30% between 2020 and 2021. This suggests that BTC may be somewhat

connected with other variables during certain periods, but its overall impact is

still relatively small.

We also examine the N ETi, which represents the difference in overall di-

rectional connectivity between the TO and FROM variables. The results show

that BTC is frequently a shock receiver, but primarily became a shock emitter

between 2020 and 2021. This means that during this period, BTC was more

likely to transmit shocks to other variables than to receive them.

Moreover, we look at the NPDT graphs, which illustrate the degree of pair-

wise directional predictability between variables. We notice a sharp increase in

the NAQ-BTC graph starting in 2020, making NAQ the asset with the most connection to BTC. We also notice some connections between BTC and VIX,

but with a negative correlation. Unlike the previous graph, we see a peak in

2018 that quickly decreases and then another peak in 2020 until the end of our

studied timeline. We also observe a similar trend in the GOLD-BTC graph,

with the peak starting in 2020 and quickly decreasing. However, we do see a

slight increase, or rather a new formation of a peak, at the end of our studied

period.

Upon initial examination, there appears to be no indication of any significant

relationship between BTC and the other variables studied. However, a closer

examination reveals a modest connection between BTC and the other factors,

with a peak in connectedness observed between 2020 and 2021. This period is

particularly noteworthy, as it marked a time of increased usage and interest in

BTC since its creation. This theme is recurrent throughout the paper and will

be further explored in subsequent sections. We also noticed this similar trend

in the previous study.

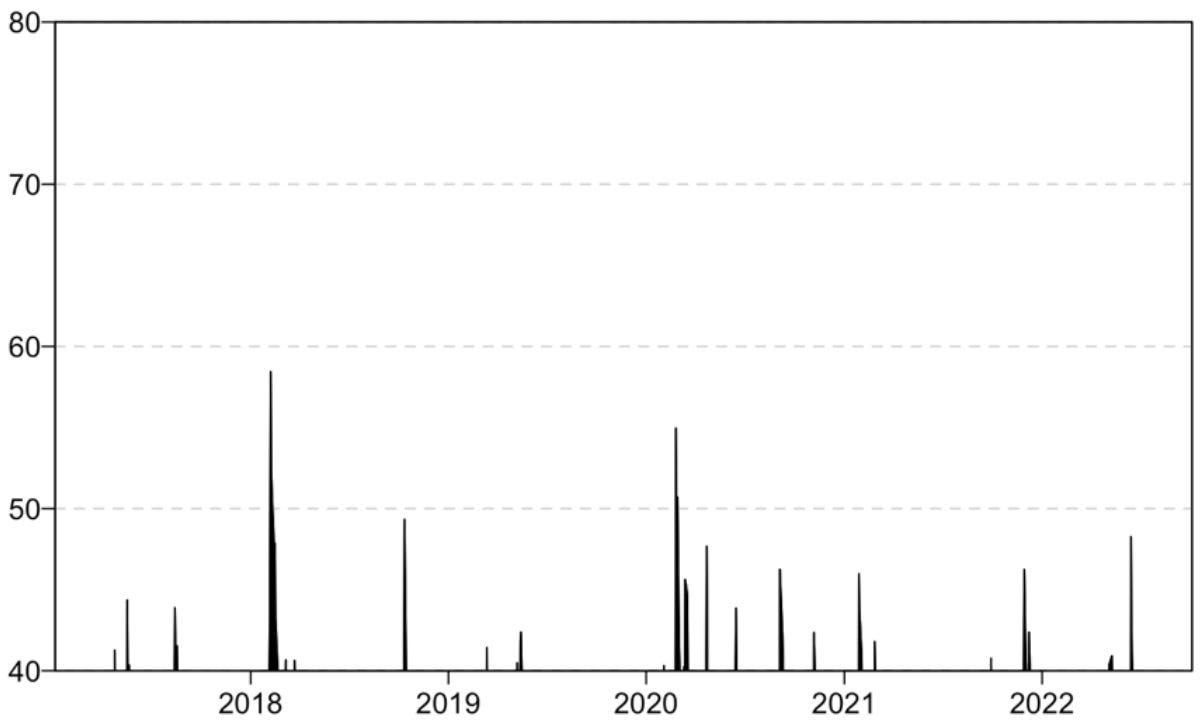

We proceed on to investigate the Total connectedness index (TCI), which

measures the average impact of all factors on the forecast error variation of a

single variable across time. We can see that there are two significant peaks: the

first occurs in 2018 and stays just under 60%, and the second occurs in 2020

and peaks at about 55%. We notice that the time period when we observe the

most spikes is between 2020-2021.

The difference in overall directional connection between TO and FROM

the other variables is represented by the NETi, which is the next step. The

findings indicate that whereas BTC was initially a shock emitter between 2020

and 2021, it is now largely a shock absorber. Similar patterns can be seen in

the TO and FROM graphs as well.

In order to identify which series has a higher or lower influence on the other,

the Net Pairwise Directional Connectedness Measure (NPDC) was used. The

findings indicate that connection increased most significantly between 2020 and

2021. Particularly, NAQ and BTC were found to have the most influence.

The graphs’ research also demonstrates that BTC had a negligible impact on

GOLD during the time period under consideration, reaching its highest influence

around 2020 before reverting to its earlier levels from 2021 until the present.

On the WTI and BTC graphs, we can see a similar peak, although the impact

is considerably less significant this time around.

We also assessed the network plots that showed the NPDC and PCI. The

two network diagrams don’t clearly or strongly depict any relationships between

BTC and the other factors studied.

Multivariate Portfolio Analysis

We delve into the analysis of multivariate portfolios, incorporating BTC and

other variables in our study, with a nuanced analysis catering to three distinct

investor risk profiles. Tables provide essential metrics such as the mean, rep-

resenting the average value over a given period, and the standard deviation,

elucidating variability around the mean.

Commencing with the minimum variance portfolio, tailored for risk-averse in-

vestors, we note GOLD commanding the largest share at 55%, followed by NAQ

and DXY at 20% and 19%. DOW and WTI contribute negligibly, and notably,

BTC is conspicuously absent.

Transitioning to the minimum correlation portfolio, crafted for those vigilant

about correlation, BTC makes its entrance with a 14% allocation, ranking as

the fourth largest weight. DXY (26%), DOW (23%), and GOLD (16%) take

the lead, while WTI and NAQ closely follow with 12% and 9%, respectively.

Finally, delving into the minimum connectedness portfolio for investors con-

cerned about network stability, BTC claims the highest percentage at 17%,

surpassing GOLD and WTI at 18%, while the remaining variables stand at

16%. Graphs vividly illustrate BTC’s pivotal role in network stability, with the

minimum connectivity score consistently higher.

Examining cumulative returns, we find that portfolios incorporating BTC

outperform those without. Notably, the minimum connectedness portfolio ex-

hibits superior performance, followed by the minimum correlation portfolio and

the minimum variance portfolio.

Moreover, our study delves into statistical nuances, exploring the signifi-

cance level (”5%”) and confidence level (”95%”) crucial in statistical hypothesis

testing. We emphasize the importance of these levels in understanding the

probability of rejecting null hypotheses and constructing confidence intervals.

HE, denoting Hedge Effectiveness, is elucidated, and the p-value is high-

lighted for its significance in assessing the statistical significance of the relation-

ship between analyzed variables.

From the graphs, we can see that BTC is the asset that will be most crucial

for preserving the stability of the entire network because it has the highest

minimum connectivity score. The MCP averages around 0.2 with a drop towards

0 between 2020 and 2021, while the MVP for bitcoin is consistently close to 0.

Lastly, we see that the MCoP averages around 0.2 throughout, with a few minor

variations. The MCP, MVP, and MCop are plotted on the cumulative return

graph next. The 3 remained largely below 1 until 2021, when MCoP barely

breached it before restarting the decline at the end of our time period.

These results indicate that if BTC were to experience a shock or disruption,

it could have a significant impact on the entire cryptocurrency market. On

the other hand, assets with lower minimum connectedness scores may be less

important for overall network stability.

Looking at the minimum of the three portfolios discussed above, we can see

that the MCoP portfolio is the most performant, followed by MCP and finally

MVP. This indicates that portfolios that included BTC outperformed those that

did not.

Finally, we will look at the cumulative return graphs, which depict an invest-

ment’s performance while accounting for both capital gains (or losses) and the

reinvested dividends or other payments that were received during the time pe-

riod. Globally, we see that, with the exception of BTC-GOLD and BTC-WTI,

portfolio pairs containing Bitcoin performed significantly better than other port-

folio pairs. We also notice that the graphs that demonstrate better performance

have very similar graphs with the same peaks along the timeline.

Conclusion

This study investigates the volatility spillover effects of Bitcoin and traditional

assets using a variety of methodologies. Its findings can help investors and reg-

ulators understand the diversification benefits and risks associated with adding

Bitcoin to their portfolios. To capture the complexities of volatility spillover

dynamics, the study employs methodologies such as Dynamic Total Connect-

edness analysis, Net Total Directional Connectedness, Multivariate Portfolios,

and DCC-GARCH models. The findings indicate that while BTC may be con-

nected to other variables at times, its overall impact remains small. Regarding

BTC’s role in investor portfolios, portfolios containing around 15.5% BTC gen-

erally outperformed portfolios containing no BTC. Overall, this study provides

useful insights into the relationships between BTC and the various variables

investigated, as well as their effects on one another.

References

[Ede79] Louis H Ederington. “The Hedging Performance of the New Futures

Markets”. In: Journal of Finance 34 (1979).

[KS93] Kenneth F. Kroner and Jahangir Sultan. “Time-Varying Distribu-

tions and Dynamic Hedging with Foreign Currency Futures”. In:

Journal of Financial and Quantitative Analysis 28 (1993).

[Xio15] Han L. Xiong Z. “Volatility spillover effect between financial markets:

evidence since the reform of the RMB exchange rate mechanism”. In:

Financial Innovation 1 9 (2015).

[Mik18] Alexey Mikhaylov. “Volatility Spillover Effect between Stock and Ex-

change Rate in Oil Exporting Countries”. In: International Journal

of Energy Economics and Policy 8 (2018).

[O18] ̈Ozdemir O. “ue the volatility spillover in the cryptocurrency markets

during the COVID-19 pandemic: evidence from DCC-GARCH and

wavelet analysis”. In: Financial Innovation 8 12 (2018). doi: https:

//doi.org/10.1186/s40854-021-00319-0.

[KS19] Anoop Kumar and Anandarao Suvvari. “Volatility spillover in crypto-

currency markets: Some evidences from GARCH and wavelet anal-

ysis”. In: Physica A: Statistical Mechanics and its Applications 524

(2019). doi: 10.1016/j.physa.2019.04.154.

[ACG20] Nikolaos Antonakakis, Ioannis Chatziantoniou, and David Gabauer.

“Refined Measures of Dynamic Connectedness based on Time-Varying

Parameter Vector Autoregressions”. In: Journal of Risk and Finan-

cial Management 13 (2020). doi: 10.3390/jrfm13040084.

[CH20] Yeguang Chi and Wenyan Hao. “A Horserace of Volatility Models for

Cryptocurrency: Evidence from Bitcoin Spot and Option Markets*”.

In: (2020).

Volatility spillover: the transfer of instability from one market to another. It occurs when

a change in volatility price in one market has a delayed impact on volatility price in another

market that is greater than the local market effects.

Is Bitcoin a Safe Haven?

Introduction In recent years, the cryptocurrency industry has experienced significant growth and increased sophistication. Despite the financial crisis of 2022, the market capitalization of Bitcoin remains high, four times that of 2020. This growth has