Is Bitcoin a Safe Haven?

Exploring the Interconnectedness of Bitcoin

Introduction

In recent years, the cryptocurrency industry has experienced significant growth

and increased sophistication1. Despite the financial crisis of 20222, the market

capitalization of Bitcoin remains high, four times that of 20203. This growth has

led researchers to examine the spillover4 effects between Bitcoin and traditional

financial markets.

Several studies have explored the relationship between Bitcoin and other

asset classes. Henriques and Sadorsky (2018) [HS18] used GARCH models to

find that replacing Gold with Bitcoin in an investment portfolio would benefit

even risk-averse investors. Urquhart (2018)[Urq18] found a relationship between

investor attention to Bitcoin and its volatility and volume. Lyer (2022) [Iye22]

found an approximate 14-18% spillover between Bitcoin and the global equity

markets. Risk spillover between Bitcoin and the traditional financial market

was also detected in Zhang et al.(2021)[Zha+21]. Similar results were also seen

in Qarni et al.(2019)[Qar+19] which studied this relationship exclusively related

to the US stock market.

Previous studies, such as Bouri et al. (2017)[Bou+17], found that Bitcoin

can function as an impact hedge and a safe haven against fluctuations in en-

ergy commodity indices, but not against non-energy commodities. Selmi et al.

(2018) [Men+18] found that Bitcoin operates as a hedge, safe haven and di-

versifier against the volatility of oil prices, similar to Gold. Moreover, Corbet

et al. (2018) [Cor+18] suggested that Bitcoin is largely unaffected by tradi-

tional financial assets, but may provide diversification benefits for short-term

investors.

The present study focuses on evaluating the level of interconnection and

potential for spillovers between Bitcoin and other asset classes. As a result, we

investigate the following questions:

How strong are the spillovers between Bitcoin and other asset classes, and

have they increased over time?How correlated are movements between Bitcoin and traditional markets?

Has this correlation changed over time?Can Bitcoin provide diversification benefits to traditional investors?

Empirical Methodology

We implement the Generalized Vector Autoregressive connectedness approach

based on Diebold and Yilmaz (2012)[DY12], which builds on Sims’ (1980)

Vector Autoregressions and Pesaran and Shin’s (1998)[Sim80] and Koop et

al’s (1996)[KPP96] generalized prediction error variance decompositions. This

method evaluates the dynamic links between multiple variables by first ”shock-

ing” one variable and observing the response of all other variables.

The effects of a shock in variable i are then accumulated and subtracted from

the shocks in variable −i. This results in the net directional connectedness

illustrating the influence that variable i has on the other assets. That is, if

variable i is influencing other variables more than is being influenced by them,

it is driving the market, while the opposite means that it is driven by the

market. However, such an analysis will mask the influence across pairs of assets.

Therefore, we compute the net pairwise directional connectedness that provides

additional insights into the intra-asset patterns. Last but not least, the dynamic

connectedness relationships can be traced over time via rolling window VAR

estimation.

To demonstrate the average impact of a shock in one series on others, we use

the total connectedness index (T CI), which is divided into the total directional

connectivity ”TO others” and ”FROM others”. The net total directional con-

nectedness (N ETi) depicts the net effect on the network, with a positive value

indicating that series i is a net shock transmitter and a negative value indicating

it is a net shock receiver.

To gauge the shock levels, we resort to the net pairwise directional con-

nectedness measure (N P SOij ), which states if series i has a larger (or smaller)

impact on series j than series j has on series i. To determine the extent of

domination of each series, we use the net pairwise transmission plot and the net

influence index.

We are interested in finding out the level of domination for each series. To

do this, we use the Net Pairwise Transmission (N P T ) plot which shows how

many series each series i dominates. In a network with k series, one series

can dominate a maximum of k − 1 series. The N P T plot summarizes the net

transmission mechanism of each series.

In addition, we use the Net Influence Index, which is similar to the Net Pair-

wise Directional Connectedness (N P DC) plot but shows changes in percentage

rather than levels.

Lastly, we use Network plots which show the NPDC and the Percentage

Change in Connectivity (PCI). These plots give us a visual representation of the

relationships between assets, displayed as arrows on the chart. We also look at

the net influence index (INF), which is equivalent to the net pairwise directional

connectedness plots, emphasizes percentage changes rather than levels.

Dataset and Empirical Results

Data Description

In this study, we investigate the implied connectedness of the return of Bitcoin

(BTC) with respect to six other financial indices that are classified into three

asset classes: equities, precious metals and foreign exchange rates. The BTC

return connectedness is the primary variable of interest in this analysis. As

proxies for the stock market returns, we utilize the Dow Jones Industrial Av-

erage (DOW) and the NASDAQ (NAQ) composite index. The volatility in the

stock market is represented by the CBOE Volatility Index (VIX). The foreign

exchange rates are represented by the U.S. Dollar Index (DXY), which is an

index of the value of the United States dollar relative to a basket of foreign

currencies. The Gold index (GOLD) serves as a proxy for the precious metals

asset class, and West Texas Intermediate (WTI) represents the commodities

asset class.

The sample data in this study comprises of daily time-series data from 2017

to 2022, which spans a five-year period and includes Bitcoin variations over that

time. This period extends from the perceived maturity of Bitcoin to its recent

surge in popularity and increased adoption as a digital currency.

Empirical Results

We initially analyze the Total connectedness index (TCI), which evaluates the

average impact of all factors on the forecast error variance of a single variable

over time. The table displays the percent connectedness impact between dif-

ferent variables. Each row represents the impact one variable has on another,

and the end column labeled ”TO” shows the impact of the other variables to a

specific variable. The end row labeled ”FROM” shows the impact of a specific

variable on the other variables. The previous last row, labeled ”NET,” repre-

sents the difference between the TO and FROM columns. Finally, the last row

labeled ”NPT” shows how many series a specific series dominates. The table

provides valuable information for analyzing the relationships between different

variables and their impacts on one another.

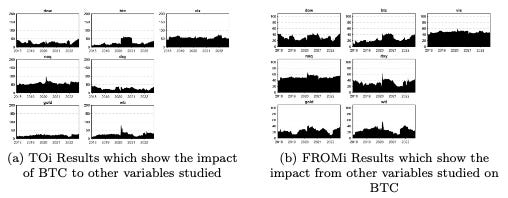

The results reveal that BTC has a minor or negligible effect on the other

series studied, and vice versa. The average influence of BTC on the other

variables in the series is approximately 25%. Additionally, (T Oi) graphs show

that BTC has an average influence of 30-40% on the other variables analyzed,

with a peak influence of 50% between 2020 and 2021. We also evaluate the

(F ROMi) graphs, which reveal that other series have a sizable impact on BTC,

with a peak influence of 40% between 2020 and 2021. Finally, we examine

the N ETi, which represents the difference in overall directional connectivity

between TO and FROM the other variables. The results show that BTC is

frequently a shock receiver, but primarily became a shock emitter between 2020

and 2021.

Upon initial examination, there appears to be no indication of any significant

relationship between BTC and the other variables studied. However, a closer

examination reveals a modest connection between BTC and the other factors,

with a peak in connectedness observed between 2020 and 2021. This period is

particularly noteworthy, as it marked a time of increased usage and interest in

BTC since its creation. This theme is recurrent throughout the paper and will

be further explored in subsequent sections.

Next, we analyze the Net Pairwise Directional Connectedness Measure (N P SO)

to determine which series has a greater or lesser impact on the other. We exam-

ine the NPS0ij between BTC and the other six variables. The results show that

the majority of the growth in connectedness occurred between 2020 and 2021.

Notably, the greatest influence was observed between NAQ and BTC, with an

average influence of -20 between 2020 and 2021. The analysis of the graphs fur-

ther reveals that BTC had a modest impact on DXY over the analyzed period,

with a peak influence observed around 2020 before returning to previous levels

from 2021 to the present.

These findings support the hypothesis that the most significant connections

are identified between NAQ and BTC, with a weaker relationship between BTC

and DXY.

The pairwise directional connectedness plots demonstrate a recurring pattern

in the relationship between DXY-BTC and NAQ-BTC. However, a stronger

association between DOW-BTC is observed. The analysis of the plots reveals a

noticeable and substantial peak between 2020 and 2021.

The net pairwise directional transmission plots determine the number of

series dominated by the BTC series. Our focus was on the BTC graph. The

results showed that the Bitcoin series dominated two series at its minimum and

six series at its maximum point in early 2021. The graph exhibited a peak trend

during the period of 2020-2021 and had the highest average number of series

dominated during this time frame.

The net influence index (INF) was also analyzed to examine the percentage

changes between the variables. The average change between the DOW and BTC

was approximately 40%, with the highest change observed at the start of 2019

reaching over 80%. The average change between NAQ and BTC was lower than

the DOW-BTC pairing, but still reached a peak of approximately 60% in 2019

and had its largest change at 80% at the start of 2020. The GOLD-BTC pair

showed a significant peak of about 80% change at the start of the observation

period, which was re-observed towards the end of the period at slightly above

80%. A comparable peak of 80% change was observed for BTC-DXY at the

start of the observation period, but the overall average change was substantially

higher than for all other pairings investigated. Regarding BTC-WTI, a low was

observed between 2020 and 2021, but the biggest peak, near the end of 2021,

was still about 80%. Finally, for BTC-VIX, a falling trend was observed starting

in 2020 and continuing into 2022, with a lower percentage change than in prior

variable graphs. The largest points of change were observed between 2019 and

2020.

The Pairwise Connectedness Index (PCI) was also analyzed in the study.

The PCI graph was constructed to represent the bilateral relationship between

BTC and the other six variables. The results revealed a modest impact between

BTC-DXY and BTC-WTI. These relationships displayed a peak impact between

2020 and 2021. Similar impact maxima were also observed in the relationship

between BTC-VIX and NAQ-BTC. The impact of NAQ-BTC had a higher

magnitude and remained elevated compared to the pre-peak levels, reaching a

peak probability of 60% in 2022. On the other hand, the relationship between

BTC and GOLD and the Dow had less than 20% influence. These relationships

displayed a slight peak impact between 2020 and 2021, but returned to levels

lower than the pre-peak.

In our final stage of analysis, we evaluated the network plots, which depicted

the NPDC and PCI. The first network figure, the NPDC, revealed a narrow con-

nection from VIX to BTC, indicating a moderate level of connectivity between

the two. However, two wider connections were observed from BTC to DXY and

GOLD, indicating a stronger relationship between these variables and BTC. In

the PCI network diagram, a thin line between BTC and NAQ suggests a weak

connection between the two.

Based on the net pairwise transmission plot and network plots, it can be

concluded that BTC was formerly connected to all six variables under consider-

ation. Upon further examination, we found that the strongest connections were

with DXY, GOLD and VIX.

Conclusion

The results of our analysis over the period of 2017-2022 show that Bitcoin is

becoming increasingly influenced by other variables such as the NASDAQ Com-

posite Index, the US Dollar Index and the CBOE Volatility Index. Our study of

Bitcoin’s effect on these variables during its peak period of 2020-2021 leads us

to question the link between Bitcoin’s volatility or risk and these variables. This

means that Bitcoin and the other assets listed before have a stronger link and

greater spillover than previously thought. As a result, we conclude that Bitcoin

cannot be considered a diversification or safety agent in relation to the assets

evaluated in this study. Further investigation of the volatility connectivity links

between these variables may result in the development of a well-constructed

portfolio. In future studies, we aim to provide a more comprehensive under-

standing of these connections.

References

[Sim80] Christopher Sims. “Macroeconomics and Reality”. In: Econometrica

48.1 (1980), pp. 1–48. doi: https://EconPapers.repec.org/RePEc:

ecm:emetrp:v:48:y:1980:i:1:p:1-48.[KPP96] Gary Koop, M.Hashem Pesaran, and Simon M. Potter. “Impulse

response analysis in nonlinear multivariate models”. In: Journal of

Econometrics 74.1 (1996), pp. 119–147. doi: https://doi.org/10.

1016/0304-4076(95)01753-4.[DY12] Francis X. Diebold and Kamil Yilmaz. “Better to give than to re-

ceive: Predictive directional measurement of volatility spillovers”.

In: International Journal of Forecasting 28.1 (2012), pp. 57–66. doi:

https://doi.org/10.1016/j.ijforecast.2011.02.006.[Bou+17] Elie Bouri et al. “On the hedge and safe haven properties of Bitcoin:

Is it really more than a diversifier?” In: Finance Research Letters

20 (2017). doi: 10.1016/j.frl.2016.09.025.[Cor+18] Shaen Corbet et al. “Exploring the dynamic relationships between

cryptocurrencies and other financial assets”. In: Economics Letters

165 (2018). doi: 10.1016/j.econlet.2018.01.004.[HS18] Irene Henriques and Perry Sadorsky. “Can Bitcoin Replace Gold in

an Investment Portfolio?” In: (2018). doi: 10.3390/jrfm11030048.[Men+18] Walid Mensi et al. “Is Bitcoin a hedge, a safe haven or a diversi-

fier for oil price movements? A comparison with gold”. In: Energy

Economics 74 (2018). doi: 10.1016/j.eneco.2018.07.007.[Urq18] Andrew Urquhart. “What causes the attention of Bitcoin?” In: Eco-

nomics Letters 166 (2018), pp. 40–44. doi: https://doi.org/10.1016/

j.econlet.2018.02.017.[Qar+19] Muhammad Qarni et al. “Inter-markets volatility spillover in U.S.

bitcoin and financial markets”. In: Journal of Business Economics

and Management 20 (2019), pp. 694–714. doi: 10.3846/jbem.2019.

8316.[Zha+21] Yue-Jun Zhang et al. “Risk spillover between Bitcoin and con-

ventional financial markets: An expectile-based approach”. In: The

North American Journal of Economics and Finance 55 (2021), p. 101296.

doi: https://doi.org/10.1016/j.najef.2020.101296.[Iye22] Tara Iyer. “Cryptic Connections: Spillovers between Crypto and Eq-

uity Markets”. In: International Monetary Fund (2022). doi: https:

//www.imf.org/en/Publications/global- financial- stability- notes/

Issues/2022/01/10/Cryptic-Connections-511776.

https://www.forbes.com/advisor/investing/cryptocurrency/crypto-market-outlook-forecast/

https://beincrypto.com/crypto-crash-2022-2008-financial-crisis-how-industry-turn-around/

https://coinmarketcap.com/charts/

A spillover in economics is a financial occurrence in one context that occurs as a result of

something else in a seemingly unrelated situation.