Unraveling NFT Pricing Complexity

In-Depth Insights from Picture-for-Profile (PFP) Collections

Introduction

Non-Fungible Tokens (NFTs) have emerged as a groundbreaking phenome-

non with the potential to revolutionize various industries, particularly in the

realm of digital assets. They are units of data stored on a blockchain certifying

the uniqueness and distinctiveness of a digital asset and are reshaping the way

we perceive digital creations in fields such as art, gaming, music, and collectibles.

They have earned significant attention in early 2021. Within the first four

months of 2021, the NFT market surpassed a trading volume of 2 billion USD.

On December 2, 2021, the market witnessed a historic sale with Pak’s NFT artwork, ”The Merge”, fetching an astounding $91.8 million, further amplifying

the significance and impact of NFTs in the art market and beyond. However,

at the middle of 2022 the NFT market started facing some challenges, leading

to a substantial decline in trading volume activity.

One category among all the spectrum of NFTs categories that has gained

remarkable prominence is the picture-for-profile. PFPs represent digital avatars

or profile images that users can adopt across various online platforms and social

media networks. BAYC, one PFP collection, is held by a few notable NBA

stars, singers and television hosts. Azuki’s NFT profile pics sold out in three

minutes and Okay Bears sold out all 10,000 NFTs in a day, bringing in a daily

record of $18 million in sales volume.

Focusing on this narrative, this research paper aims to contribute to the current knowledge landscape by conducting a thorough investigation into the

intricate determinants influencing the pricing of NFTs, with a specific focus on

the picture-for-profile category. Through an in-depth analysis of five distinct

NFT collections falling under this category, we seek to uncover the underly-

ing internal and external factors that propel market dynamics and ultimately

determine the intrinsic value of these digital assets.

In the subsequent sections of this research paper, we present the literature

review, providing an overview of the current knowledge of NFTs, yet still limited,

the methodology we used in this paper, as well as the database that we built,

the results for our 5 analyzed PFP collections, the discussion of these results

and the conclusion.

Literature Review

This literature review aims to explore the methodologies and findings of

several studies that shed light on the multifaceted realm of NFTs. By delving

into these different aspects, we aim to provide a comprehensive understanding

of the NFT ecosystem, its complexities, and its potential implications.

NFTs, or non-fungible tokens, represent tradable rights that can be securely

recorded as ownership tokens on the blockchain through the use of smart con-

tracts (Ko et al. 2022). While there are various definitions of NFTs, a simplified

explanation is that they are tokens that certify the uniqueness of digital assets

(Kapoor et al. 2022).

However, in order to gain a better understanding of these digital assets,

it is helpful to categorize them based on their different types. (Nadini et al.

2021) has identified six distinct groups of non-fungible tokens, namely Art,

Collectible, Games, Metaverse, Utility and Other. Although this categorization

provides a broad framework for discussing NFTs, the “Other” category is quite

vague and lacks precision. To notice this limitation, we can cite (Mazur, n.d.),

a research paper that delves into the risks and returns of NFTs and explores

various financial use cases, such as trading, liquidity mining, farming, collateral-

based loans, and fractional NFTs. These use cases, if classified, would all fall

under the broader classification of “Other”, not being very precise.

Upon comprehending the categorization of NFTs and their use cases, we

looked into the various factors that can influence the price of an NFT. In this

regard, (Kaczynski and Kominers 2021) examined the creation of NFT value

through several key aspects; the scarcity, which stems from the unique nature

of an NFT, making it highly desirable and valuable, the rarity, which is enhanced

when some creators intentionally limit the number of tokens they produce, the

authenticity, which involves the verification of an NFT’s uniqueness, the prove-

nance, which is related to the ownership history and transaction records of an

NFT, the popularity, which plays a important role when the collection is as-

sociated with renowned artists or celebrities, or when it has gained significant

attention on social media, and lastly, utility, which is an important factor to

analyze whether an NFT offers more practical use cases beyond being a mere picture.

Furthermore, the influence of visual features in the price of NFT is a well-

explored subject in the literature. For example, (Mekacher et al. 2022) thor-

oughly investigated the number of distinctive attributes linked to each NFT, as

well as the distribution of these attributes within the collection. Building upon

this idea, (Krasnoselskii, Madhwal, and Yanovich 2023) collected all attributes

from an NFT collection, measuring their rarity and proposing a rarity score. In

contrast, a different approach was taken by (Nadini et al. 2021) that considered

the overall image of each NFT instead of analyzing individual attributes sepa-

rately. Finally, (Alexander and Chen 2022) introduced the concept of grouping

NFTs with similar attributes, creating clusters and conducting separate analyses

for each cluster.

While these factors primarily encompass elements intrinsic to the NFT or

its collection, there are also external factors that may influence the NFT’s price.

For example, (Borri, Liu, and Tsyvinski 2022) investigated the influence of the

cryptocurrency market as well as traditional assets such as equity, commodities,

and currencies on NFT prices.

Finally, we looked into various economic models to modelize the price of

each NFT. When we have a number of observations on sales of objects that,

although individually unique, have some degree of commonality, and trades

are infrequent, all characteristics that we find in an NFT sale, we can apply

the Hedonic Regression (Galbraith and Hodgson 2018). The Hedonic method

was first proposed by (Court 1939) and then largely used and improved in the

literature, with a focus on the Real Estate and Art market. (Agnello, n.d.)

estimated the returns as well as the effects of various features of the paintings,

like their size, who is the author, where it was auctioned, the medium of painting

(e.g. oil, acrylic on canvas, panel, board, Masonite. . . ) on price. (Meese and

Wallace 1991) estimated house price for some cities in the United States of

America, considering for the feature variable the number of bathrooms and

bedrooms, finished square footage, total number of rooms, dwelling age, and for

the dummy variable the presence or absence of pools, fireplaces, assumability of

mortgage, mortgage type and zoning type.

Besides, this model incorporates external factors and features that can af-

fect house price, such as the impact of crime risk of property values (Linden

and Rockoff 2008), the relationship between the undergrounding electricity and

telecommunication network with house prices (McNair and Abelson 2010), and

the impact of Noosa national park on surrounding property values (Pearson,

Tisdell, and Lisle 2002).

However, it is important to note that it is not possible to include all potential

characteristics that may influence the price of an asset. (Epple 1987) highlighted

the issue of omitted variable bias, which poses a significant problem in hedonic

regression models. To mitigate this problem, one approach is to adapt the

hedonic model, which typically analyzes the price of a single asset, and instead

consider a pair of sales. The repeat sales model, proposed and improved by (Case

and Shiller 1987), is a powerful model that can estimate the house price index

without explicitly considering the attributes of the house. An adapted version of the Case and Shiller index is currently utilized by the S&P 500 to calculate

the house price index. While there is limited literature linking this method to

the NFT market, (Borri, Liu, and Tsyvinski 2022) employs the repeat sales

method to construct an overall index for the NFT market.

In parallel to the economic models, the emergence of machine learning and

artificial intelligence has provided opportunities to develop ML models for pre-

dicting NFT prices. (Nadini et al. 2021) employed a deep convolutional neural

network to extract the image feature and analyze their influence. Similarly,

(Mekacher et al. 2022) used the same approach to identify latent variables that

potentially drive the relationship between rarity and price. Moreover, (Jain,

Bruckmann, and McDougall, n.d.) built a recurrent neural network to uncover

the underlying factors affecting NFT prices, while (Alexander and Chen 2022)

applied ML techniques, such as random forest algorithm, to predict the NFT

rarity based on their attributes.

With that in mind, we can construct mathematical models to estimate the

price of NFTs and find the factors that influence its valuation, but it is also

important to consider alternative perspectives. According to (Kapoor et al.

2022), directly modeling NFT valuation as a mathematical economic system

may not be the most accurate approach. Instead, it should be viewed as a so-

cial phenomenon involving marketing schemes, the recognition and popularity

of the NFT. The role of social media has a significant impact on that valu-

ation and it emerges as a crucial factor of the NFT price. This perspective

aligns with previous research that has examined the impact of Twitter on stock

market prediction (Bollen, Mao, and Zeng 2011), highlighting the relevance of

social media in financial contexts. Additionally, this same article references the

Efficient Market Hypothesis, which suggests that stock markets are primarily

influenced by new information, such as news, rather than relying solely on past

and present prices. These insights encourage a holistic approach that incor-

porates social factors, market sentiment, and the timely incorporation of new

information alongside mathematical modelling when analysing NFT valuations.

Empirical Methodology

Before delving into the mathematical model, we believed that it was es-

sential to establish our own categorization framework to gain a comprehensive

understanding of the NFT landscape, as it follows:

1) Social / Membership: NFTs that can grant access to exclusive events and

communities.

2) Metaverse: NFTs that can represent plots of land on which it is possible to

construct buildings or organize events. This digital space enables activities such

as hosting online exhibitions or facilitating massive multiplayer video games.

3) Gaming: NFTs that are associated with any digital item from the domain

of online games. It can be in-game items, characters, skins, maps, tickets, etc.

4) Proof of ownership of a specific physical or digital item: NFTs that have

a physical artwork related in real life.

5) Financial NFTs: NFTs that represent fractional ownership of physical

assets (real estate, cars. . . ), stocks and bonds, futures and options contracts,

virtual currency-backed NFTs.

6) Music: NFTs that represent albums or music releases.

7) Domain name: NFTs that can simplify decentralized domains, such as

wallet addresses.

8) Pictures for profiles (PFPs): NFTs that were created to be displayed on

social media profiles.

9) Collectibles: NFTs that have been created to be used and are attached

to a project.

10) Photography: NFTs that represent unique photographs, often taken and

edited digitally.

11) Comics: NFTs that represent unique comic book pages, often featuring

digital art and storytelling

12) 3D Sculptures: NFTs that represent unique 3D sculptures, created using

3D modeling software and often animated or interactive.

13) Digital Paintings: NFTs that represent unique digital paintings, created

using digital tools and softwares.

14) Artistic Videos: NFTs that represent unique video works of art, often

including animation, motion graphics, and sound.

15) Mixed Media Art: NFTs that represent unique digital pieces that com-

bine multiple types of media, such as painting, sculpture, photography, and

digital design.

With the aid of this categorization framework, we can develop a comprehen-

sive overview of the NFT ecosystem, facilitating analysis of the potential factors

that may impact its pricing. We have classified these factors into two distinct

categories: internal and external.

Internal Factors:

1) Artist Popularity/Brand Recognition: This variable refers to the fame

and recognition of the artist or creator behind the NFT. The more popular or

well-known the creator, the more valuable the NFT may be.

2) Quality of Artwork/Visual Features: This variable refers to the aesthetic

value of the artwork or visual features of the NFT. The higher the quality and

appeal of the artwork or visual features, the more valuable the NFT may be.

This can also be seen as the value or appeal of the artwork from a market

perspective.

3) Number of NFTs (Scarcity): This variable refers to the number of NFTs

available in circulation. The scarcer the NFT collection is, the more valuable it

may be.

4) Rarity: This variable is similar to the previous one and refers to how

unique the characteristics in the NFT are. The more unique the attributes in

an NFT, the more valuable it may be.

5) Blockchain Technology: This variable refers to the blockchain chosen for

creating and maintaining the NFT. The more popular and widely used the

chosen blockchain, the more valuable the resulting NFT may become.

6) Added Utility: This variable refers to any additional benefits or uses that

the NFT may have beyond its intrinsic value. For example, if the NFT grants

access to exclusive content or events, it may be more valuable.

7) Historical Significance (OG NFTs): This variable refers to the historical

significance of the NFT, especially if it was one of the first NFTs ever created.

The more historical significance the NFT has, the more valuable it may be.

8) Process: This variable refers to the process of creating a collection with

respect to the various methods used by the artist.

External Factors:

1) Social Media: This variable refers to the impact that social media may

have on the value of the NFT. If the NFT is popular on social media platforms,

it may be more valuable.

2) Market Trends/Demand: This variable refers to the current market trends

and demand for NFTs. If there is a high demand for NFTs, the value of the

NFT may increase.

3) Economic Conditions: This variable refers to the overall economic con-

ditions, such as inflation, that may affect the value of the NFT. For example,

during an economic downturn, the value of NFTs may decrease.

By incorporating both internal and external factors, we aim to gain an ex-

tensive understanding of the various elements that can shape the value and de-

sirability of NFTs within the studied collections. We gathered the data focusing

on the most prominent PFP collections in terms of volume, namely CryptoP-

unk , Bored Ape Yacht Club, Mutant Ape Yacht Club, Azuki, CloneX, and

Moonbirds. We opted to exclude CryptoPunk from our analysis because it was

one of the first NFT collections launched in 2017, before the implementation

of the ERC-721 token protocol that is used nowadays. Consequently, relevant

historical sales data for that collection was not found, leading to its omission

from our research.

Initially, we turned to Etherscan, an Ethereum block explorer and analyt-

ics platform, to obtain the data, since all the collections mentioned are on the

Ethereum blockchain. While etherscan provided information on sales and mint-

ing, and we got the mint data for our analysis, we encountered an issue when

sales were conducted in currencies other than ETH, not being accurately repre-

sented. Furthermore, the traits data for each NFT was not available on Ether-

scan, leading us to search for another option.

Our next approach involved exploring Alchemy, a web3 developer platform,

to find the desired data. Unfortunately, we were unable to retrieve the traits

data for the collections, prompting us to quickly dismiss this option. Conse-

quently, we continued our search for a reliable source of NFT data.

Although Reservoir had the historical sales data, we could not rely on that

third option due to the presence of missing data when manually verifying the

information.

Ultimately, we turned to NFTPort, where we successfully obtained all the

desired data except for the mint price and mint date, which we got on Ether-

scan. For each collection, we retrieved the traits of all the NFTs, the historical sales data for each token ID, as well as the buyer and seller addresses. Ad-

ditionally, we obtained the sale prices in both ETH and USD, although, in

some instances, only the ETH price was available. To address this, we uti-

lized the historical price of that token to calculate the USD price, available at

www.coingecko.com/en/coins/ethereum.

We made a slight adjustment to the historical sales data to suit our model’s

requirements. Specifically, we observed that some NFTs were sold multiple times

on the same day with price differences of less than 5%. Such cases indicated that

these sales were driven purely by speculative motives. To streamline our dataset

and eliminate potential noise from speculative transactions, we decided to retain

only the first sale of each NFT on a given day, excluding any subsequent sales.

In addition to the NFT data, we also gathered various time series for further

analysis, such as the S&P 500 index from Yahoo Finance, the Federal Funds Rate

available at https://www.newyorkfed.org/markets/reference-rates/effr, and the

ETH price data from CoinGecko.

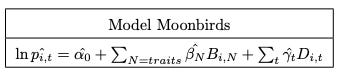

As mentioned in the literature review, we modeled our problem as a hedonic

model (Court 1939):

Before proceeding with the model, we first addressed the problem of mul-

ticollinearity, which occurs when two or more independent variables are highly

correlated, making it challenging to isolate their individual effects on the de-

pendent variable. To tackle this problem, we calculated the correlation matrix

for all independent variables in the dataset. This matrix reveals the pairwise

correlation between each pair of independent variables, ranging from -1 to +1,

where -1 indicates a perfect negative correlation, +1 represents a perfect positive

correlation, and 0 suggests no correlation.

Next, we established a threshold of ±0.7 for the correlation coefficient, and

if the correlation between two variables exceeded this threshold, we excluded one of them from the model. By doing so, we retained the most relevant and

informative predictors while mitigating the impact of multicollinearity.

To determine the coefficients of the Hedonic model, we adopted the Ordinary

Least Squares method (OLS), which minimizes the sum of the squared differ-

ences (residuals) between the observed dependent variable and the predicted

values generated by the linear equation.

It is worth noting that our NFT’s characteristics remain constant over time,

and thus our vector of features, denoted Bi,N , is the same for each period.

Greenlees (1982), Mark and Goldberg (1984) analyzed this special case when

the feature vector varies over the time, but we don’t need to treat our problem

in this way.

Following the coefficient estimation, we examined the correlation and causal-

ity between the regression coefficient related with the time, denoted as γt, and

three other time series: S&P 500 index, FED rate and ETH price.

To measure the correlation between two series, we utilized the Pearson Test,

which is a statistical test to assess the strength and direction of two variables, by

calculating the Pearson correlation coefficient (r). This coefficient ranges from -

1 to +1, where -1 represents a perfect negative linear relationship, +1 represents

a perfect positive linear relationship, and 0 indicates no linear relationship.

For measuring causality between two series, we employed the Granger Test,

which is a statistical test that helps to determine whether one time series can

predict another time series, revealing the temporal relationship between vari-

ables and assessing the predictive power of past values from one variable on

another one.

Results

Bored Ape Yacht Club

Proceeding with the methodology described in the previous section, we

started by analyzing the correlation between all the traits. For the Bored Ape

Yacht Club, we didn’t find any correlated traits (with the correlation matrix

coefficient higher than 0.7).

Following the steps, we ran our Hedonic Model to find the appropriate model to predict the collection price, considering only the statistically significant coeffi-

cients. We found that all coefficients were statistically significant at a significant

level of 0.05, but the coefficients related to the background feature.

We continued the analysis by measuring the linear relationship between the

estimated coefficients and its rarity and finally we ran a Pearson test and a

Granger test to verify the correlation and causality of the temporal estimated

coefficient and three other temporal series.

Mutant Ape Yacht Club

This collection is a particular one because it has a different type of mint for

some specific token ids: the last 20000 NFTs can only be minted if you have a

BAYC NFT (a detailed explanation will be given in the next section). Our first

approach was to treat all 30000 NFTs as equal.

We didn’t find any statistically significant coefficient.

As a second approach, we divided the collection into two: the first being

the 10000 NFTs (Token ID 0 to 9999) and the next 20000 (token id 10000 to

29999). The explanation of that division will be given in the next section.

For the first group, we found only 8 significant coefficients and we didn’t

continue the analysis for this first batch.

For the second group, we found the following model, with 764 statistically

significant coefficients, but with 260 not statistically significant coefficients.

Because of the high number of statistically insignificant coefficients, we de-

cided to not proceed the analysis for the second sample either.

Azuki

For the Azuki collection, we found 14 pairs with the correlation matrix co-

efficient higher than 0.7 and thus we excluded one of each pair from our feature

vector.

For the Hedonic Model, at a significant level of 0.05, we found that only the

temporal coefficients are significant to predict the price.

Following with the Pearson test and Granger test, we found that the esti-

mated temporal coefficients are correlated with the ETH price, S&P500 and

with the Fed Rate, and we found a causality with the S&P500 index with lag

2, 3, 4, and 5.

Since we didn’t have significant coefficients for the features, we didn’t verify

the relationship between them and rarity.

CloneX

For the CloneX collection, we found 8 correlated pairs of features and we

excluded one feature of each pair from our feature vector.

For this collection, we didn’t have a sufficient number of statistically signif-

icant coefficients. Only for these cases of features (Table 6).

Since we didn’t have enough coefficients, we didn’t proceed with the Granger

test, nor the Pearson test.

Moonbirds

For the Moonbirds collection, we found 16 correlated pairs of features and

we excluded one feature of each pair from our feature vector.

For the model, at a significance level of 0.05 we didn’t have any statistically

significant coefficients, but at 0.10 we found the following model:

Some traits were not statistically significant (Table 8).

We continued the analysis by measuring the linear relationship between the

estimated coefficients and its rarity and finally we ran a Pearson test and a

Granger test to verify the correlation and causality of the temporal estimated

coefficient and three other temporal series.

Apart from the individual analyses of each collection, we also conducted a

comparative assessment to derive general insights. The results are presented in

the following six charts:

The first Chart represents the Number of transactions / (number of NFTs in

the collection * days since its first minting). This is a good KPI that we proposed

to analyze the frequency of transactions in a collection. It is important to notice

that if we decided to look only for the number of transactions, the number

would not be very meaningful: older and bigger collections tend to have more

transactions than newer and smaller ones. Then, with this KPI we can eliminate

these factors and normalize the number of transactions.

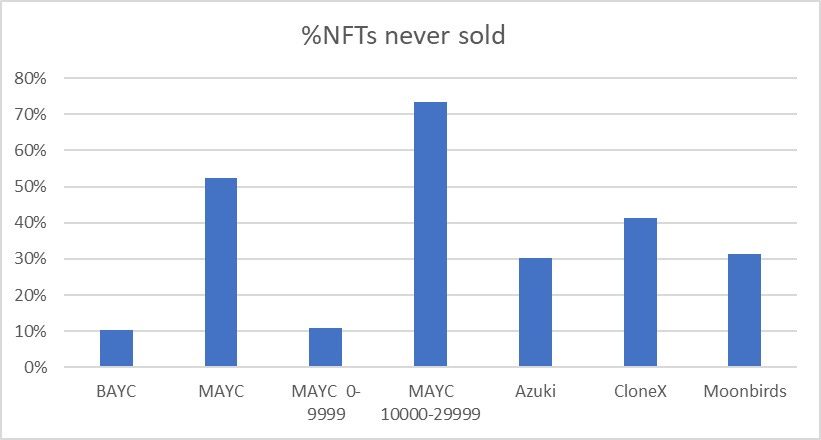

The second chart displays the percentage of NFTs in a collection that were

never sold.

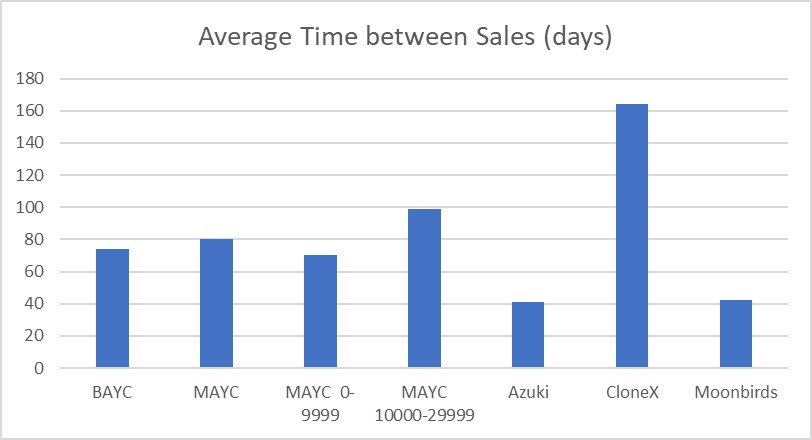

In the third chart, we observe the average time in days between sales of the

same NFT, including the time of the first sale.

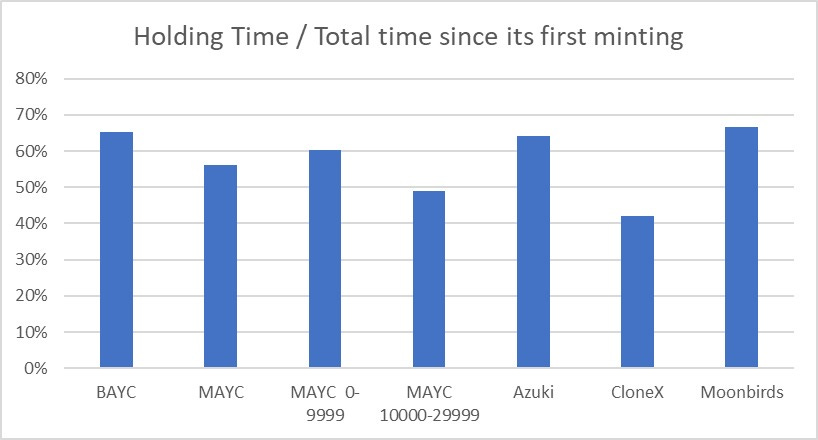

Chart four provides insights into how long people tend to keep their NFT

in their wallet. Again in this case, we proposed this KPI which we divide by

the total time since its first minting. The reason behind is that older collections

tend to have higher holding time than newer ones, because of its age.

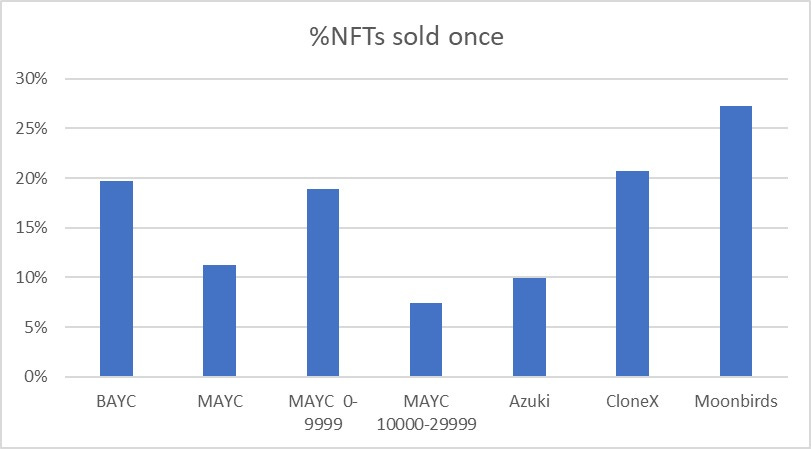

The fifth chart shows the percentage of NFTs that were sold only once.

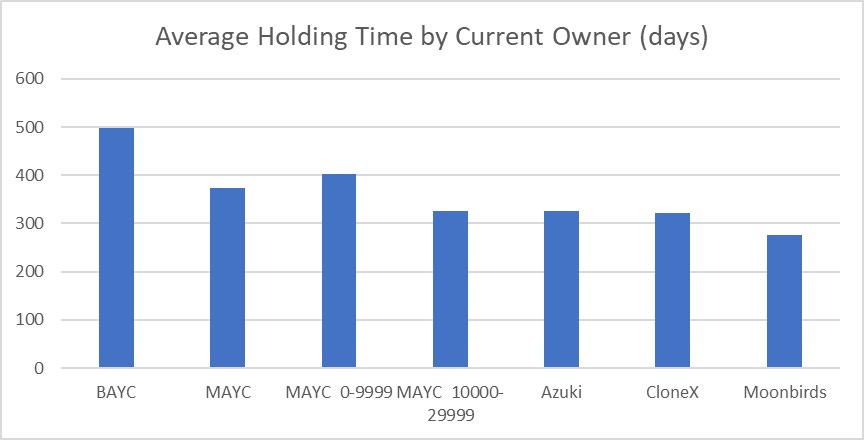

Lastly, the sixth chart highlights the holding time, which is the average time

that the actual owner of the NFT holds it.

Discussion

The findings from the analysis of the 5 PFP collections have yielded signif-

icant insights regarding our research question. They shed light on the charac-

teristics of these collections and the factors that may impact them. Notably,

for two collections (BAYC and Moonbirds), traits and aesthetics emerged as in-

fluential factors, suggesting that potential buyers consider the visual appeal of

the PFPs before making a purchase decision. On the other hand, for three col-

lections (BAYC, Azuki, and Moonbirds), external factors played a substantial

role in investors’ decision-making process. Lastly, the results for two collections

(CloneX and MAYC) were inconclusive, warranting further investigation.

Bored Ape Yacht Club and Moonbirds

Starting with Bored Ape Yacht Club (BAYC) and Moonbirds, the results

indicate that the feature vector of estimated coefficients plays a significant role

in influencing the price of NFTs, suggesting that potential buyers prioritize the

features and aesthetics of an NFT before making a purchase.

Moreover, when considering the percentage of total time that these two col-

lections were held (Figure 25), they stood out among the others. This reinforces

the idea that people value these NFTs and tend to hold them for more extended

periods because of personal preferences rather than speculative motives. No-

tably, the data showed that Moonbirds is the collection with the highest per-

centage of NFTs sold only once (Figure 26), exceeding 25%. On the other hand, BAYC is the collection where people hold onto their NFTs for the longest pe-

riod of time (Figure 27). These results provide further support to the notion

that individuals perceive NFTs from these collections as personal items of value

rather than mere speculative assets.

Looking deeper into the traits effects, we selected one trait from each collec-

tion to analyze its rarity influence. For the Bored Ape Yacht Club collection, we

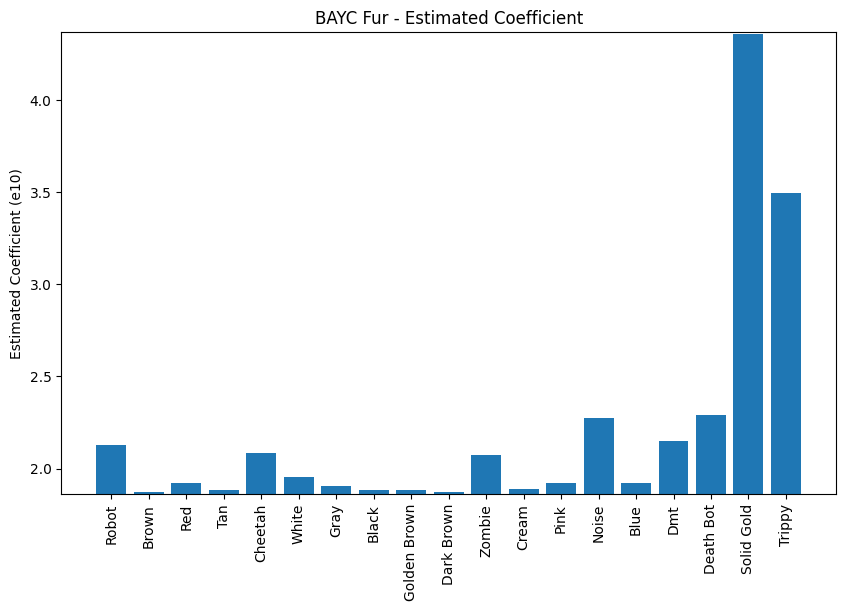

focused on the “FUR” trait. In figure 5, our findings revealed that the “Solid

Gold Fur” is the rarest feature, accounting for less than 2% of the total NFTs

in the collection. Additionally, when exploring the average sale price of NFTs

in a determined type of fur (Figure 7), the Solid Gold Fur emerged as the most

expensive by a significant margin.

We attempted then to establish a linear relationship between rarity and price

(Figure 8), but the results were not highly conclusive (R2 = 0.16). That result

was led by some cases like the “Blue Fur”, which exhibited an average frequency

within the sample, and surprisingly possessed the lowest average price. This

complexity in the relationship between rarity and price hindered a strong linear

approximation.

Interestingly, all the estimated coefficients from our analysis were positive,

indicating that the presence of any trait, regardless of which one, would pos-

itively impact the predicted price of the NFT. This suggests that having a

particular trait, irrespective of its rarity, contributes to higher price predictions

for the NFT.

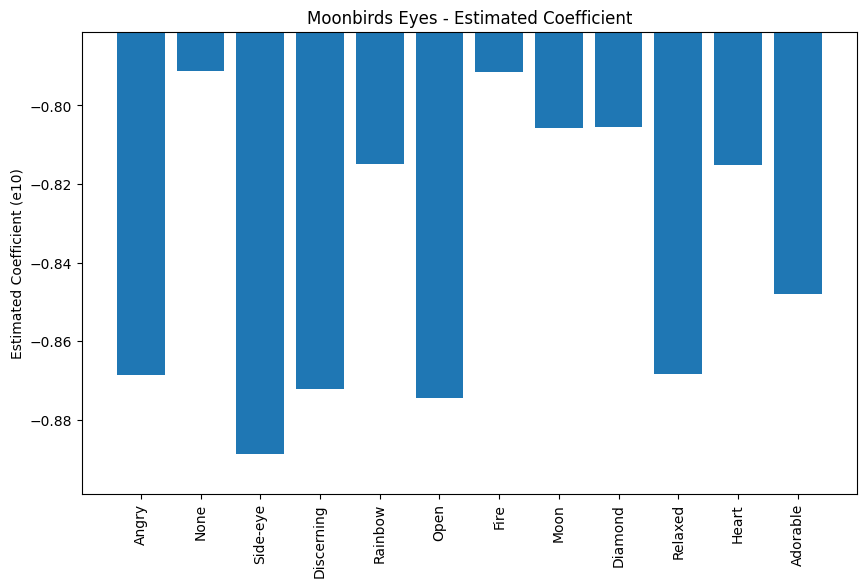

For the Moonbirds collection, we focused on the “eyes” trait to analyze

the relationship between rarity and price. Again in this case, we observed a

visual relationship between rarity and price, specifically, the “rainbow”, “fire”,

“moon”, “diamond”, and “heart” eyes were the scarcest within the collection

(Figure 18) and consequently, we found that NFTs featuring these unique eyes

traits, along with the “none” category, commanded the highest prices (Figure

20). However, trying to find a linear relationship to elucidate that relationship

was not very explanatory (Figure 21 shows R2 = 0.26).

Intriguingly, the behavior of the estimated coefficients differed from what we

found for the BAYC collection. For Moonbirds eyes, eyewear, headwear, and

outerwear, the coefficients were negative, indicating a downward pressure on the

predicted price. Conversely, the beak coefficients were all positives, suggesting

a positive influence on the price prediction. The coefficients for background,

body, and feathers were a mix of positive and negative values. For example,

legendary guardian, legendary emperor, legendary professor, legendary crescent,

legendary brave, and legendary sage feathers had positive coefficients, indicating

a preference for these unique features. On the other hand, feathers in colors like

gray, blue, white, purple, black, red, brown, prink, green, and none showed

negative coefficients, implying a lesser price impact, possibly due to their more

common occurrence.

Overall, that interaction between price and traits in the Moonbirds collec-

tions was very intriguing, as we exemplified with the eyes coefficients that were

all negatives, including the “none”, meaning that with or without this trait,

the price would decrease. This finding wasn’t entirely clear in our analysis and warrants further investigation to fully grasp the underlying factors involved in

it.

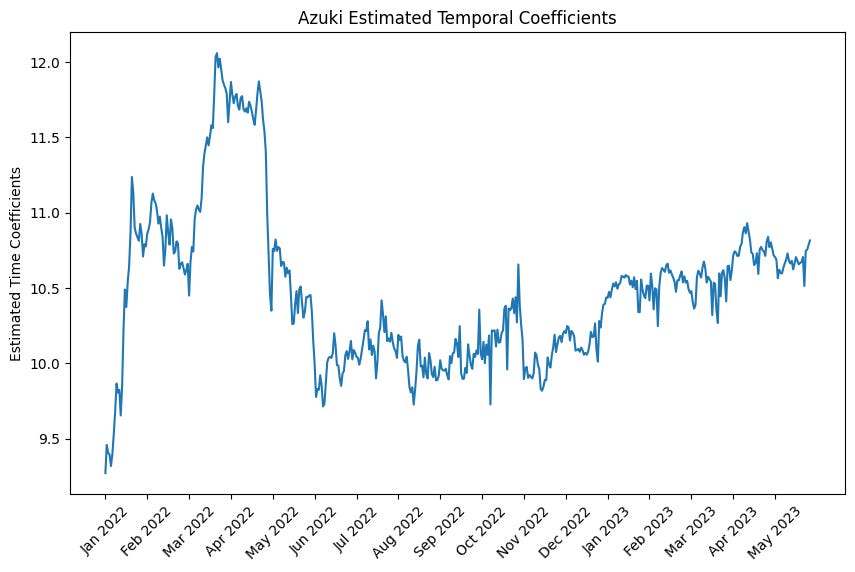

In our model, we not only identified the statistical significance of the feature

coefficients, but we also found that the temporal coefficients were significant.

After subjecting these coefficients to the Pearson correlation test, we observed

a strong correlation relationship between them and the three series we chose

to analyze: the ETH price, the S&P 500 index, and the Fed Rate. With the

ETH price, it is possible to see that the behavior of BAYC and Moonbids tem-

poral coefficients are similar to the ETH price behavior during certain “crypto

crashes” like the Luna crash in May 2022 and the FTX crash in November 2022.

However, it is essential to emphasize that correlation does not imply causation,

and we cannot establish a direct causal link based on these correlations.

Furthermore, we found correlations with two additional macroeconomic vari-

ables: the S&P5500 and the Fed Rate. This indicates that movements beyond

the NFT environment exhibit similar behavior to that observed within these

collections. While the exact causal mechanisms remain uncertain, these corre-

lations highlight the interconnectedness between broader economic conditions

and NFT pricing.

During the Granger causality test, for the BAYC collection, the analysis

yielded no evidence of causality between the temporal coefficients and the time

series proposed, even when exploring different time lags. In contrast, for the

Moonbirds collection, the causality test indicated a significant causation between

the temporal coefficient and the ETH price, with a lag of 5 time periods (Table

9). This implies that fluctuations in the ETH price play a contributory role in

shaping price variations within the Moonbirds collection.

This result is in line with (Ante 2021), who used data between January 2018

and April 2021 to demonstrate the impact of cryptocurrency markets on the

NFT market, finding that NFT sales were influenced by Bitcoin and Ether price

shocks. Furthermore, (Dowling 2021b) reinforces this result, as his exploration

of the NFT market in early 2021 suggested that cryptocurrency pricing may

provide valuable insights into NFT pricing patterns.

However, it is important to approach these findings with a degree of cau-

tion. Causality in complex systems like the NFT market can be influenced by

numerous interrelated factors, and the precise mechanisms at play may require

further investigation.

Azuki

In our investigation of the Azuki collection, we made intriguing discoveries

regarding the significance of feature and temporal coefficients. Different from

the first two collections, the feature coefficients were not statistically significant,

indicating that within this collection, people seem to be less concerned about

specific NFT features and more focused on market conditions and various in-

ternal and external factors. This observation suggests that the Azuki collection

may lean towards being a speculative collection, where buyers are driven by

investment opportunities rather than individual NFT characteristics.

Supporting this notion, Figure 24 reveals that Azuki exhibits the lowest

average time between sales, 41 days, suggesting that individuals tend to buy and

sell Azuki NFTs quickly, treating them more like short-term investments rather

than holding them for extended periods. In addition to that, we proposed a new

KPI that also corroborates with that result (Figure 22): number of transactions

per number of nfts in the collection per day since its first minting. Azuki was

on top of the other collections in that chart, showing its high trade frequency.

As we did not observe any statistically significant feature coefficients, we

did not explore their relationship with the rarity of traits within the Azuki

collection. Instead, we proceeded with correlation and causality tests to delve

further into the dynamics at play.

During our analysis, we discovered correlations between the three series we

examined with the temporal coefficients in the Azuki collection. Additionally,

the Granger causality test revealed that the S&P500 at lag 2,3,4,or 5, exhibited

a significant correlation with the Azuki NFT price. These findings align with

our previous observations, suggesting that investors may closely monitor the

behavior of the S&P500 to inform their investment decisions concerning specific

Azuki NFTs. Consequently, movements in the S&P500 are likely to influence

the overall price of the Azuki collection.

This connection between a market indicator and the Azuki NFT price high-

lights the speculative nature of the collection, where external market factors

hold sway over the NFT pricing dynamics.

That result diverged from the findings by (Aharon and Demir 2021), who

investigated NFTs’ connectedness with other financial assets during COVID-

19, concluding that NFTs have an independence from common asset classes

(equities, bond, currencies, gold, and oil).

The observed divergence in findings may be attributed to the difference in

the time frames analyzed. Aharon and Demir studied the period from January

2018 to June 2021, while Azuki’s first mint occurred in 2022. As the NFT market

rapidly evolves, early stages might not reflect its current state and hence, the

NFT landscape at the beginning of the study might differ significantly from the

present scenario. Therefore, considering the time gap is crucial to account for

the dynamic nature of the NFT market.

CloneX

Our next examination was CloneX and it posed unique challenges different

from the other collections. Regrettably, we did not find any statistically signifi-

cant coefficients in our model. This suggests that the model we proposed might

not be the most suitable for this particular collection.

One notable aspect of CloneX is its status as the oldest collection among all

those we studied, with over two years since its first minting. However, surpris-

ingly, approximately 40% of CloneX NFTs remain unsold (Figure 23). This sig-

nificant number of unsold NFTs introduces complexities that impact the model’s

precision in capturing all influences, particularly concerning the features coef-

ficients. Since only 60% of the NFTs were sold at least once, the model only considers the features of those sold NFTs, leaving some traits that were never

sold unaccounted for. This limitation has a detrimental effect on the reliability

of the coefficients within the model.

Regarding temporal coefficients, we observed that CloneX exhibited the

highest value in the Average Time Between Sales, reaching 164 days (Figure

24) . This implies that CloneX NFTs are not traded frequently, making it chal-

lenging to incorporate the temporal aspect into the model due to the scarcity

of sales data.

Given these limitations and the lack of sufficient statistically significant co-

efficients, we made the decision to not pursue further tests of correlation and

causality. Instead, we acknowledge the uniqueness of the CloneX collection and

the difficulties it presents in analyzing its pricing dynamics.

Mutant Ape Yacht Club

MAYC stands out as another distinct collection that posed its own unique

challenges during our analysis. Running the model for all NFTs within the

collection (token ID from 0 to 29999), did not yield any statistically significant

coefficients. Similar to CloneX, MAYC’s peculiarities influenced these results.

One notable aspect of MAYC is that over 50% of its NFTs were never

sold (Figure 23), surpassing even the percentage observed in CloneX. Conse-

quently,certain traits within MAYC were never considered in our model, im-

pacting the precision of feature coefficients. This lack of sales data for a signif-

icant portion of the collection introduced complexities in the comprehension of

the price dynamics.

Furthermore, the average time between sales for Mutant Ape Yacht Club

NFTs is 80 days (Figure 24), outstanding the duration observed in BAYC,

Azuki, and Moonbirds collections. That infrequency of sales further complicated

the inclusion of temporal effects in the model, making it challenging to capture

the dynamics of pricing fluctuations.

Given these challenges, our initial analysis, a naive one, faced limitations

in fully grasping the pricing behavior within the MAYC collection. However,

acknowledging these unique characteristics motivates us to explore alternative

approaches and refine our methodology.

We made a deliberate division, creating two distinct sub-collections.The first

collection comprises token IDs ranging from 0 to 9999, while the second collec-

tion includes token IDs from10 to 29999. The division is not arbitrary; it aligns

with significant differences in the minting process and requirements for each

group.

The first 10000 MAYC NFTs were generated through the usual process of AI

image generator, where a random vector of features creates unique NFTs that

can be minted by anyone in the community. This approach is consistent with

the typical NFT minting process, making this subset a representative sample of

conventional NFTs within the MAYC collection.

The second group, however, follows a distinctive protocol for minting. To

acquire a Mutant Ape Yacht Club NFT from this subset, individuals need to possess a Bored Ape Yacht Club NFT, and additionally, they require a special

element called “Serum”, available in two types: number 1 and number 2. With

these prerequisites met, individuals can mint their MAYC NFT, whose process

will follow the same steps as the first group, through an AI image generator.

This strategic division enabled us to examine two distinct categories within

the MAYC collection, shedding light on the contrasting dynamics between con-

ventional minting and the exclusive requirements for minting within the second

group.

During our analysis of the first part of the MAYC collection (token IDs

0-9999), we encountered an unexpected result. Despite a high percentage of

NFTs sold, Figure 23 shows only 11% of NFTs in that group remained unsold,

a considerable number of transactions per NFT per time of existence (Figure

22), and a low average time between sales (Figure 24), we did not find any

statistically significant coefficient.

These characteristics led us to expect a similar behavior to that of BAYC and

Moonbirds collections, where the feature and temporal coefficients significantly

influenced price predictions. However, as we have seen, this was not the case.

At this point, we have not yet determined the reasons behind this outcome, and

further investigation is needed to understand the implications fully.

On the other hand, the second part of MAYC collection (token IDs 10000-

29999) exhibited a behavior more akin to the BAYC and Moonbirds collections.

These NFTs stand out as unique with its way of minting, fostering a sense of

pertinence among collectors that mint it. As a result, a significant portion of

these MAYC NFTs were never sold (over 70% according to Figure 23).

In addition to that, Figure 22 reveals infrequent trading activity for these

NFTs, suggesting that collectors tend to hold onto their NFTs and this sub-

collection has the second-highest average time between sales (Figure 24), behind

CloneX. This aspect emphasizes the collector-oriented nature of the owners of

these NFTs. Despite all these characteristics, we still observed some temporal

influence in the predicted price (there were some significant temporal coefficients

in our model), indicating that those who decide to sell their minted NFTs may

consider market conditions in their decision-making.

Due to the absence of a continuous time series for our temporal coefficients,

with some coefficients turning out to be statistically insignificant, we made the

decision to not proceed with the correlation and causality tests. Similarly, we

encountered some features coefficients that lacked significance, resulting in miss-

ing coefficients. As a consequence, we opted against verifying the relationship

between the rarity of traits and their estimated coefficients.

The limitations posed by these missing coefficients in both temporal and fea-

ture coefficients prevented us from conducting further analyses to explore corre-

lations and causal relationships. Recognizing these constraints, we acknowledge

the need for a more comprehensive dataset to gain deeper insights into the

dynamics and influences governing the NFT pricing within the collection.

In conclusion, the results emphasized that the aesthetics and features of

NFTs have a significant impact on the pricing of BAYC and moonbirds, and

people tend to hold NFTs they appreciate for more extended periods. The Moonbirds collection, despite having fewer transactions overall, witnessed a sub-

stantial percentage of NFTs sold only once, showcasing the initial intention of

buyers to retain these items in their wallets. The Azuki collection appeared as

a speculative collection, with external market factors influencing its pricing dy-

namics more than specific NFT features. CloneX and MAYC presented unique

challenges in analyzing their pricing behavior due to their particularities and

their data availability.

Conclusion

In this research, we conducted a comprehensive analysis of five PFP collec-

tions, identifying the factors influencing the pricing dynamics of these digital

assets. Through rigorous examination, we made significant findings that con-

tributed to our understanding of the NFT market.

Firstly, we discovered that certain collections possess a speculative factor,

wherein the NFT prices are influenced by external market conditions. For

instance, the Azuki collection demonstrated a strong correlation between its

NFT prices and the S&P 500 index, indicating a close relationship between

the broader economy and the pricing dynamics of these NFTs. On the other

hand, Moonbirds exhibited a causal relationship with fluctuations in the ETH

price, suggesting that market movements in the Ethereum cryptocurrency play

a contributory role in shaping price variations within the collection.

Secondly, we observed that some collections had an appeal factor, where

NFT prices were influenced by intrinsic factors such as aesthetics features. No-

tably, Bored Ape Yacht Club and Moonbirds collections showed correlation

between specific NFT features and their prices, indicating that potential buyers

prioritize visual appeal and unique traits before making a purchase decision.

In all cases where a temporal effect was significant in the model, the ETH

price, S&P500, and Fed Rate exhibited correlations with the temporal coeffi-

cients estimated.

However, while our research yielded valuable insights for some collections,

we also encountered challenges in constructing a precise model for the Mutant

Ape Yacht Club and CloneX collections. The complexity and uniqueness of

these collections hindered a robust analysis. As a result, further investigation

is required to provide explanations for the difficulties encountered and to gain

deeper insights into the dynamics driving the pricing behavior within these

collections.

Moving forward, future research could apply the repeat sales method to the

Azuki collection, given its speculative nature, and also for MAYC and CloneX,

trying to identify the underlying pricing patterns and relationships.

In addition to traditional econometric approaches, future research papers

could employ machine learning models to analyze NFT pricing dynamics. Lever-

aging machine learning algorithms could help identify complex patterns and rela-

tionships between NFT characteristics, external factors, and transaction prices.

Another approach for exploration is the influence of social media platforms on NFT pricing and price volatility. Treating NFT price volatility as a social

phenomenon rather than merely a mathematical or economic problem would

provide a more comprehensive understanding of NFT market behavior and the

role of social influence.

Lastly, expanding the research to explore other NFT categories beyond PFPs

is essential for gaining a holistic view of the NFT market. Each category may

possess distinct characteristics, driving factors, and market dynamics. Conduct-

ing similar analyses for other categories, such as virtual real estate, digital art,

and gaming NFTs, would enrich the overall understanding of the entire NFT

ecosystem. By broadening the scope of the study, we can capture the diver-

sity and complexities of NFT markets, contributing to a more comprehensive

knowledge base for the digital asset space.

References

Agnello, Richard J. n.d. “INVESTMENT RETURNS AND RISK FOR

ART:” EASTERN ECONOMIC JOURNAL.Aharon, David Y., and Ender Demir. 2021. ”NFTs and asset class spillovers:

Lessons from the period around the COVID-19 pandemic.” Finance Research

Letters 47: 102515.Alexander, Carol, and Xi Chen. 2022. “Rarity Metrics for Non-Fungible

Tokens.” SSRN Electronic Journal. https://doi.org/10.2139/ssrn.4242042.Ante, Lennart. 2021. ”The non-fungible token (NFT) market and its rela-

tionship with Bitcoin and Ethereum.” FinTech 1, no. 3: 216-224.Borri, Nicola, Yukun Liu, and Aleh Tsyvinski. 2022. “The Economics of

Non-Fungible Tokens.” SSRN Electronic Journal. https://doi.org/10.2139/ssrn.

4052045.Case, Karl, and Robert Shiller. 1987. “Prices of Single Family Homes Since

1970: New Indexes for Four Cities.” w2393. Cambridge, MA: National Bureau

of Economic Research. https://doi.org/10.3386/w2393.Court, Andrew. 1939. “Hedonic price indexes with automotive examples”,

in “The Dynamics of Automobile Demand”, General Motors, New York, pp.

98.Dowling, Michael. 2021. ”Is non-fungible token pricing driven by cryptocur-

rencies?.” Finance Research Letters 44: 102097.Epple, D. 1987. Hedonic prices and implicit markets: Estimating demand

and supply functions for differentiated products. Journal of Political Economy,

95(1), 59–80.Galbraith, John, and Douglas Hodgson. 2018. “Econometric Fine Art Val-

uation by Combining Hedonic and Repeat-Sales Information.” Econometrics 6

(3): 32. https://doi.org/10.3390/econometrics6030032.Greenlees, J. S. 1982. An Empirical Evaluation of the CPI Home Purchase

Index, 1973-1978, Journal of the American Real Estate and Urban Economics

Association, 10:1, 1-24.Jain, Shrey, Camille Bruckmann, and Chase McDougall. n.d. “NFT Ap-

praisal Prediction: Utilizing Search Trends, Public Market Data, Linear Re-

gression and Recurrent Neural Networks.”Kapoor, Arnav, Dipanwita Guhathakurta, Mehul Mathur, Rupanshu Yadav,

Manish Gupta, and Ponnurangam Kumaraguru. 2022. “TweetBoost: Influence

of Social Media on NFT Valuation.” arXiv. http://arxiv.org/abs/2201.08373.Kaczynski, Steve, and Scott Duke Kominers. 2021. “How NFTs Create

Value.” Harvard Business Review. November 10, 2021. https://hbr.org/2021/

11/how-nfts-create-value.Kireyev, Pavel, and Ruiqi Lin. n.d. “Infinite but Rare: Valuation and

Pricing in Marketplaces for Blockchain-Based Nonfungible Tokens.”Ko, Hyungjin, Bumho Son, Yunyoung Lee, Huisu Jang, and Jaewook Lee.

2022. “The Economic Value of NFT: Evidence from a Portfolio Analysis Us-

ing Mean–Variance Framework.” Finance Research Letters 47 (June): 102784.

https://doi.org/10.1016/j.frl.2022.102784.Krasnoselskii, Mikhail, Yash Madhwal, and Yury Yanovich. 2023. “KRA-

MER: Interpretable Rarity Meter for Crypto Collectibles.” IEEE Access 11:

4283–90. https://doi.org/10.1109/ACCESS.2023.3236080.Linden, Leigh, and Jonah E Rockoff. 2008. “Estimates of the Impact of

Crime Risk on Property Values from Megan’s Laws.” American Economic Re-

view 98 (3): 1103–27. https://doi.org/10.1257/aer.98.3.1103.Mazur, Mieszko. n.d. “Non-Fungible Tokens (NFT). The Analysis of Risk

and Return.”Mark, J.H. and M.A. Goldberg, 1984, Alternative housing price indices: An

evaluation, AREUEA Journal 12, 3&49.McNair, Ben, and Peter Abelson. 2010. “Estimating the Value of Under-

grounding Electricity and Telecommunications Networks.” Australian Economic

Review 43 (4): 376–88. https://doi.org/10.1111/j.1467-8462.2010.00608.x.Meese, Richard, Wallace, Nancy, 1991. Nonparametric estimation of dy-

namic hedonic price models and the construction of residential housing price

indices. Real Estate Econ. 19 (3), 308–332. http://dx.doi.org/10.1111/1540-

6229.00555.Mekacher, Amin, Alberto Bracci, Matthieu Nadini, Mauro Martino, Laura

Alessandretti, Luca Maria Aiello, and Andrea Baronchelli. 2022. “Hetero-

geneous Rarity Patterns Drive Price Dynamics in NFT Collections.” arXiv.

http://arxiv.org/abs/2204.10243.Nadini, Matthieu, Laura Alessandretti, Flavio Di Giacinto, Mauro Martino,

Luca Maria Aiello, and Andrea Baronchelli. 2021. “Mapping the NFT Revolu-

tion: Market Trends, Trade Networks, and Visual Features.” Scientific Reports

11 (1): 20902. https://doi.org/10.1038/s41598-021-00053-8.Pearson, L.J., C. Tisdell, and A.T. Lisle. 2002. “The Impact of Noosa

National Park on Surrounding Property Values: An Application of the Hedonic

Price Method.” Economic Analysis and Policy 32 (2): 155–71. https://doi.org/

10.1016/S0313-5926(02)50023-0.Schnoering, Hugo, and Hugo Inzirillo. 2022. “Constructing a NFT Price

Index and Applications.” arXiv. http://arxiv.org/abs/2202.08966.Wen, Audrey Elizabeth, and HoiYat Wong. 2021. “Bidder and Seller

Strategies in Online Auctions: A Review:” In . Guangzhou, China. https:

//doi.org/10.2991/assehr.k.211209.325.