Atka 2023 predictions

A few reasons to keep faith in crypto

2022 has shown to be quite a typical bear market year. We started off hopeful, partly in denial that the November 2021 pull back was a real signal of markets turning, fueled by narratives of extended market cycles. As the volumes started to die down, and the first large liquidations hit, things really began turning sour towards April-May.

Since then, the entire crypto market has been an endless flow of liquidations, scandals, project dying, scams… which remains quite typical of a market rationalization. Big bad actors are being pushed out, taking the good ones down with them.

Usually, it is during these tough times that we can identify the projects that are hard at work, building what will be the narratives of the next few years. Betting on these projects while there is still blood in the street has proven to be quite a lucrative move for many investors who are still deeply invested in this space.

With these nine predictions, we want to present to you how we anticipate 2023 unfolding.

Enjoy the read !

1/ Serious surviving builders will thrive in the next bull run

A sustained bear market is a wonderful opportunity for well-funded projects to build, away from the noise & FUD. New gems will have a hard time fundraising in 2023, but those who successfully raised in 2021 and 2022 will be perfectly positioned to ride the next bull run.

Among the myriad of fundraising rounds over the past two years, the few projects that truly build, execute their vision and find their product market fit will survive and thrive. Their ability to identify an addressable market, maintain a healthy treasury management (ie: avoiding “too good to be true” stablecoin yields while downsizing to extend runway if needed), as well as the appropriate tokenomics design & token distribution strategy will be key.

On the other hand, a lot of less assiduous projects will vanish this year, on the back of:

poor treasury management (e.g. storing assets on FTX 😱)

inaction leading to a slow death

token launch at the wrong timing and/or without any market-making (can literally bring your token to 0)

inability to pivot your project until you meet an addressable market

wrong time-to-market (including “being right too early”)

lack of security audits / bug bounties… leading to exploits and distrust

Taking the example of DeFi, have a look to the 10 largest fundraisings in 2018 ($m, as per DefiLlama):

Some of them collapsed, while other are fighting for survival; yet, 3 of them were the biggest winners of the latest bull:

MakerDAO: $5.2bn ATH market cap (c.$680m in January 2023)

Synthetix: $5.2bn ATH market cap (c.$550m in January 2023)

Compound: $4.3bn ATH market cap (c.$380m in January 2023)

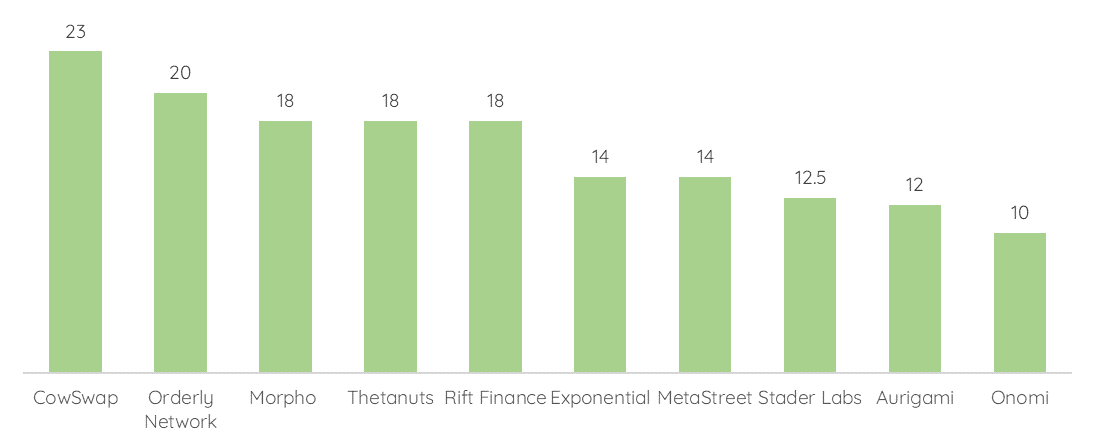

Now, a look at the top 10 early-stage projects that raised in 2022 ($m, publicly announced, as per DefiLlama):

There is a good chance that some of the biggest winners in the next cycle will come from this list. In particular, we can already witness the excellent execution for both Morpho and CowSwap as investors and early users/contributors.

The crypto market is in better shape than it was at the end of 2018, and most of the projects from the above list will be able to withstand a longer-than-expected bearish period.

2/ Bear market survivors rationalize their positions and focus on protocols or companies generating net profits

The latest bull market has witnessed competent algorithmic market-neutral traders (e.g. Three Arrows Capital, Alameda) shifting to directional trading / fundamental analysis (that requires a completely different skillset), craving for higher returns, and eventually bursting when the crypto market started to turn around. “Almost everything looks alike in a bull market” as we say, which is both true-ish and frustrating for rational investors. But when alpha gets harder to get, fundamental analysis is absolutely key to separate the wheat from the chaff.

The days of “get rich quick” schemes backed by influencers shilling projects on Tik Tok on a daily basis, as well as gleaming pitch decks with unrealistic promises are over (until the next bull market drives investors and speculators mad again). Instead, bear market investors will have to rely on actual metrics to identify and invest in the fee-generating protocols, while also ensuring that tokenomics are properly designed to drive value towards token holders.

As seen below, there is still little correlation between fees generated by protocols and how the market values these protocols. In that regard, projects like Uniswap, Lido, DYDX and GMX might be among the obvious winners of the next cycle.

Top fee-generating protocols:

Highest P/F (Price to Fees) multiples:

On the other hand, as sustainable yields will be much harder to drive, we might see the resurgence of on-chain asset managers, and a growing interest in yield-optimizing protocols. We have witnessed, in the former cycle, how sophisticated investors have disregarded yield-optimization strategies as capital was easily accessible and returns were skyrocketing. The story will be different this year.

More importantly, investors have started to understand that double digit yields in bearish times can quickly evaporate (remember the 20% yield on UST offered on Anchor). As the saying goes: if you don’t understand the yield, YOU are the yield.

3/ The crypto market decoupling will occur

Over the past few years, Bitcoin dominance [Bitcoin market cap / Total crypto market cap ratio] has slowly decreased, as new promising cryptocurrencies emerged.

Source: https://www.statista.com/statistics/1269669/bitcoin-dominance-historical-development/

Innovators have designed alternative crypto networks with faster transaction speed, smart contract execution, and more generally, different value propositions.

However, institutional investors tend to consider cryptocurrencies as a new asset class where the different cryptos were traded in a similar fashion. They used to behave as if BTC was a proxy to a tech stock, and that BTC and the rest of cryptos were similar.

An euphemism for a bear market is “market rationalization”. We believe that 2023 will be the turning point when large investors acknowledge that some cryptos (Ethereum, Cosmos, Polkadot, Solana, let alone DeFi applications...) have very different, more complex value propositions than Bitcoin, and that trading them the same way is not rational.

This will mark the Crypto Great Decoupling. Bitcoin price may see a decent recovery, correlated with a moderate activity increase, but other crypto networks like Ethereum may skyrocket.

While Lightning Network supposedly enables faster transactions over the Bitcoin network, it is slowly getting more traction, but it remains limited. Aside from Lightning Network, nothing very compelling is being built on top of Bitcoin. Bitcoin does not go beyond its store of value / decentralized payment network, which is fine, but it is probable that the next bull run will be headed by cryptocurrencies with more aspirations and potential than BTC.

The developer activity is steady on Bitcoin, while it is massively growing on other protocols.

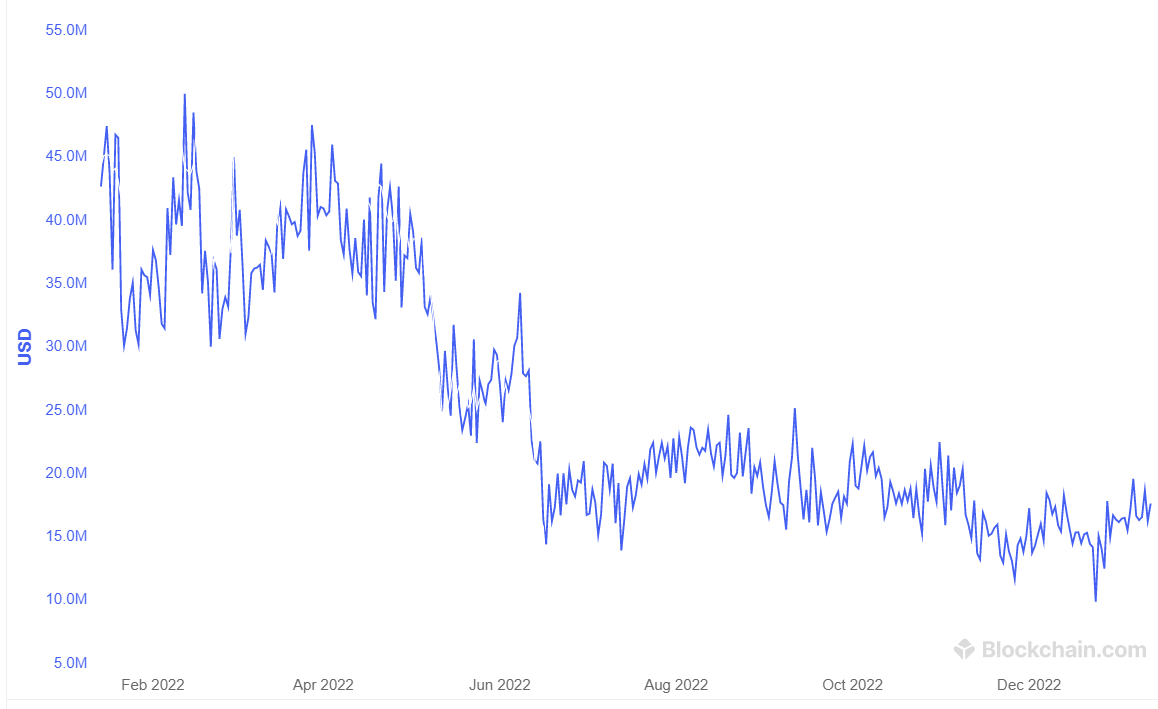

Another factor that should trigger a “decoupling” is the growing concern over Bitcoin security budget: indeed, as we can see from the chart below, the financial compensation of Bitcoin miners for securing the network is decreasing, while the hash rate is on the rise. As a result, mining firms are financially struggling, and we could fear the long term security budget for Bitcoin.

Source: https://www.blockchain.com/explorer/charts/miners-revenue

4/ Crypto users quickly switch from monolithic layer-1s to modular, application-specific chains & rollups

The bankruptcy of Celsius, Voyager, FTX in 2022 showed the considerable advantages of DeFi over CeFi. Traders withdrew their assets from Centralized Exchanges en masse, and Decentralized Exchanges, such as DYDX, saw a boost in trading volumes. This trend will surely continue in 2023.

As a result, optimizing on-chain transaction fees will become a concern for every trader, hence we expect a boom in rollup transactions.

Rollups are seen as the solutions for Ethereum to scale to the next level, and the Ethereum Developer Community is actively working to make them more and more affordable and usable in 2023.

The release of ZkSync 2.0 and Celestia this year, and better tooling for rollups should see more users & more developers building on them.

5/ Account abstraction is the most underrated crypto adoption vector in 2023

Account abstraction may not appear like a revolutionary feature, yet it might be the killer UX trick that enables mainstream crypto adoption. Account abstraction refers to the ability for blockchain transactions to be executed automatically if certain conditions are met. The implications of operations programmability are huge: for example, they’re solving important UX issues in crypto, such as the need of storing your private keys securely or signing transactions manually. Instead, we could see social recovery wallet functions, wallet permissioning systems, fully automated on-chain trading strategies, etc.

However, for this to become a reality, you must have a Programmable Account [~Smart Contract Wallet], not an Externally Owned Account [~Private key wallet]. There are ongoing debates within the Ethereum Developer community about how to deal with this transition, and several Improvement Proposals have been discussed. Account Abstraction is incorporated into Starknet and ZKSync 2.0, and we think it will be key for the adoption of those technologies in 2023, whereas Ethereum could struggle to find a consensual way of handling “legacy” EOAs.

6/ We will not see a specific crypto framework being implemented in the US or Europe

Both DeFi projects and CeFi businesses have been struggling to offer sufficient protection to retail investors, with the former having experienced numerous smart contract exploits & rug pulls and the latter being under high scrutiny following the FTX drama. Aside from FTX and Alameda, several large CeFi players have collapsed this year (BlockFi, Celsius, Blockchain.com, Voyager, to name a few).

On the other hand, regulation is progressing, but might not impact crypto players this year:

In the European Union, MiCA (Market in Crypto-assets Regulation) will take effect in 2024 (even though some EU members, like France, have already implemented a similar regulation), and won’t regulate DeFi (provided that DeFi can be regulated…)

In the US, the DCCPA (Digital Commodities Consumer Protection Act) was aimed at regulating the trading of digital assets, but is now considered as tainted (SBF was lobbying in the shadows for this regulation that would have been detrimental to DeFi protocols…). The timing for a new version of DCCPA or a new act is uncertain, and might not happen this year

To summarize, retail investors won’t have a crypto-specific legal framework to protect them, will face the risk of losing their assets stored on centralized crypto exchanges in case of new collapses, and won’t blindly rely on DeFi protocols either. So, where does that leave us?

First, DeFi markets have been maturing, and smart contract auditing is now a fully-fledged component of the crypto industry. We should expect generally fewer exploits in the space, but it will be up to the DeFi participants to carefully select the protocols they interact with. DYOR, as no regulator will do it on your behalf.

Second, the FTX/Alameda story brings to light the true power of self-custody and DeFi. It’s interesting to note that the first actor that got repaid when things went wrong for Alameda was a DeFi protocol (Abracadabra.money). Why rely on opaque centralized lenders when you can lend and borrow according to objectivized rules in DeFi? Why take the risk of depositing on a centralized exchange when you can swap securely your assets in a few clicks on CowSwap or UniSwap?

Third, on-chain analytics is shifting from compliance tools for projects to retail-facing products. We believe that products like Fire.xyz, Nansen, Dune Analytics and Glassnode (coupled with market intelligence tools like Messari) will scale and be used by investors to assess the health and reliability of DeFi protocols and interact with them securely.

2023 will be a turning point for DeFi, as it will reach its true potential in terms of security, scalability and user experience. We’ll even see a portion of TradFi jumping straight into DeFi (without the need to go through centralized platforms), with the launch of regulatory-compliant DeFi platforms like 1inch Pro and AAVE Arc.

7/ NFTs: beyond the hype, valuable use cases will emerge

Over the past few years, NFTs have had the time to go from a vague concept only a few people heard about, to being on the forefront of mainstream media, followed by experiencing an impressive burst of the over-inflated bubble that was created from a worldwide hype.

Along their journey, they have so far found a market for 2 principal applications: digital art and PFPs (collectibles with associated IP, branding…).

Digital art encompasses everything from unique digital art pieces represented by their associated NFTs, to collections of generative art like the ones promoted and distributed by ArtBlocks.

PFPs usually take the shape of randomly generated images according to certain patterns, rendering a collection of about 10,000 NFTs that collectors can identify with, displaying as their profile pictures on social media, giving them access to certain associated communities… The most popular PFP collections today being the Crypto Punks and the Bored Ape Yacht Club (BAYC).

After the stellar growth of these two verticals during 2021, a rationalization was expected alongside the rest of the crypto market. Thousands of collections were created, over 95% of which saw their value tend to 0. That being said, a vibrant ecosystem of projects still subsists today and is actually driving some heavy volumes, even during the difficult times of late last year and the beginning of 2023. This doesn’t fail to remind us of similar dynamics of the 2017 bull run when thousands of ERC20 shitcoins were created with big promises only to fail and end up being worth nothing, while a bunch of projects were actually busy building and made it through the 2018-2019 bear markets.

On the one hand, we expect these basic usage to keep growing massively, but we’re also quite eager to see new applications leveraging NFT growing and find their market fit.

We can already sense some narrative getting stronger around the concepts of:

On-chain Identity, Reputation systems and badges: leveraging transferable or non-transferable NFTs (bound to the initial receiving address) can indeed be leveraged to identify and qualify a range of addresses and accounts holding them. Coming up with smart ways to properly distribute them is a challenge with interesting use-cases. For example, Sismo offers a framework for users and communities to create dedicated badges distributed according to certain actions that an account has performed, while giving full privacy to the account. Otterspace is building an environment to greatly facilitate the onboarding of members in DAOs, based on a system of quests and NFT badges.

Lending: we’re already seeing a large increase in the usage of NFT lending protocols. The idea for the end user is to be able to get leverage by borrowing ETH against valuable NFTs. Projects like NFTfi lead the way in 2022, and new projects like KairosLoan are proposing novel lending mechanisms and better UI/UX. We think NFT lending will become much more seamless and widely used.

NFT composability: composability of different NFTs from different collections should also start to gain traction. Different projects and communities will continue partnering together to offer an enhanced experience in metaverses or gaming use-cases. You’ll be able to leverage your assets in different ways in different environments.

8/ Gaming will be the most important crypto adoption vector in 2023

Another vertical that we anticipate gaining traction this year is Gaming. Similarly to the NFT trend, 2021-2022 saw the creation of a bubble around blockchain gaming projects that was eventually rationalized. For a market used to quick code delivery and testing in a production environment, realizing the development cycle of great games is more around 4-5 years efficiently managed expectations and largely reduced project valuations.

After a few years of building, we believe 2023 will see the first sign of good traction and popularization of actually good AAA games. While obfuscating the use of blockchains in the background, they will be a perfect trojan horse to onboard a large new set of users by introducing them to the principles of wallets, tokens and NFTs, and democratizing the use and the ownership of these in-game assets.

Until now, one of the major problems with blockchain games has been that they have been focused on economic mechanics (play-to-earn and farming) that were neither fun nor interesting at all for players. We think a few major AAA games, such as Illuvium, Aurory, will actually provide engaging gaming experiences and fuel this trend.

We’ll also see the first evidence of widespread acceptance of more casual mobile games with blockchain components. Gaming studios and ecosystems will leverage the power of their communities by enabling them to co-create the games and own a part of them.

More generally, conventional gamers will be less spiteful against NFTs and crypto as they discover utility beyond the FUD and greed around them.

9/ Traction of Real World Assets on public blockchains: we’re neither there yet today, nor tomorrow

On a less enthusiastic note, we don’t expect that tokenized Real World Asset (RWA) will gain any kind of significant adoption. Whether it is the use of RWA tokens as collateral in some DeFi products or fractionalization of RWA ownership, it will fail to gain any real traction and find market fit. We’re thinking about it by drawing a connection with the trends in security tokens over the last 5 years. Many initiatives have attempted to develop platforms and solutions to represent assets with a token and trade these tokenized versions of shares, bonds, real-estate, and so on. More broadly, we believe that the idea of maintaining a bridge between the physical and digital world has been a disappointing story, and we don’t anticipate this to alter during the year of the greatest bear market this ecosystem has witnessed.